Back in June, our blog post, Meme Stocks are Easy Shorts, reported on the gradual stabilization of borrow rates for the premier meme stock, GameStop (GME), and others since their historic surges in January. The surges in GME, BB (Blackberry), and AMC were prompted by home traders rallying with other retail investors on message boards to coordinate purchasing of stocks with significant short interest, thereby inducing short squeezes.

In turn, traders with short positions in GME were subject to margin calls and forced to buy back their stock in GME, perpetuating upward price spirals. In conjunction with short squeezes, GME became virtually impossible-to-borrow (ITB) with a rate upwards of 50% during February, as just one example.

Borrow rate, or the privilege of borrowing shares, is not free, as mentioned in our blog last June. It involves borrowing a stock that an investor does not own and paying a fee, or borrow rate, which is expressed as an annual percentage. For liquid securities, these fees are low, averaging about 0.25%. However, stocks with significant short interest can become hard-to-borrow (HTB), or nearly ITB, with rates exceeding 25% for some annually. Implied borrow costs reflect the market makers’ costs of shorting in the options market.

OptionMetrics calculates the borrow rate or the costs of shorting stocks across various horizons and maturities with our latest product, IvyDB Borrow Rate. The dataset gives institutional investors and academia the ability to pinpoint short-selling pressure, analyze dynamic borrowing conditions, and improve research on short-selling positions.

Where is GME Now?

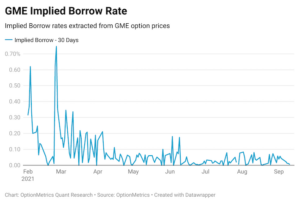

We leveraged IvyDB Borrow Rate for an update on GME. The table below plots the standardized 30-day borrow rate. Shorting costs for GME have come back down to earth with rates consistently less than 1%. In other words, the price of shorting GameStop has never been cheaper and is comparable to borrow rates for highly liquid, mega cap names.

This indicates that market in GME has become much more liquid, and a trader can buy or sell the stock with relative ease. This is likely a result due to a reduction in the total short interest on GME from levels of 42% in early 2021 to 10% currently. Additionally, we see market makers have been able to analyze retail behavior more effectively, and therefore accommodate their order flow in the options market.

While GME could rally in the future, it likely will not be a result of the short squeeze, given the changes in the dynamics of the market.

What’s Next?

GME is not what it used to be when it comes to the short squeeze, however other stocks with high short interest might be future targets for them. IvyDB Borrow Rate can be used to help to assess stocks that might be susceptible to short squeezes.

Contact us at info@optionmetrics.com for more information on IvyDB Borrow Rate.