Germany’s economic landscape stands at a critical juncture in late 2024, facing a perfect storm of challenges that could spark significant market volatility. The largest economy in Europe is grappling with a stark combination of domestic political instability—following the collapse of Chancellor Olaf Scholz’s coalition government—and looming external threats from potential U.S. trade policies accompanied by an escalation in the Russia-Ukraine War. With GDP already contracting and a potential 1% further decline on the horizon from proposed Trump tariffs, German exporters face unprecedented uncertainty. This cocktail of political upheaval, economic weakness, and trade tensions should create a volatile environment for German equities.

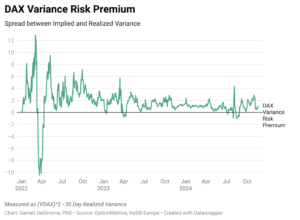

Given this challenging environment, one would expect heightened volatility risk in the DAX. A key metric for gauging how investors price this risk is the Variance Risk Premium (VRP)—the spread between implied variance and realized variance. This metric reflects the compensation investors demand for bearing volatility risk. Implied variance is derived from options pricing, while realized variance measures actual market volatility.

A positive VRP indicates that markets consistently price in more uncertainty than materializes, highlighting investors’ risk aversion. Historically, a positive VRP correlates with higher expected market returns over intermediate horizons (1–3 months), as investors who take on variance risk are rewarded with high returns.

The chart below illustrates the percentage difference between implied and realized variance on the DAX40 index. Implied variance is calculated using the squared VDAX index. Over the period from January 2020 to the present, the average VRP stands at 1.52, with a median of 1.73. Currently, the VRP sits at 1.13—below the historical average.

This relatively subdued VRP is surprising, given the widespread negativity surrounding Germany’s economic contraction and political uncertainty. However, this can be attributed to the lack of immediate, hard risk events. For example:

- The conclusion of the U.S. election has removed a significant source of uncertainty.

- While U.S. tariff threats persist, their scope and timing remain unclear.

- Snap elections in Germany are not scheduled until late February, leaving a three-month window without significant domestic political events.

The current VRP suggests that options markets have not yet priced in maximum pessimism, likely reflecting the absence of immediate catalysts. While the broader economic and political challenges create a negative narrative, the VRP offers a more neutral signal for German equities in the short term.