Future uncertainty and anxiety are two of the main drivers of implied volatility. This was apparent last month when Nvidia precipitously fell 17% upon the sudden appearance of DeepSeek. Less well reported was the effect the AI newcomer had on Nvidia’s implied volatility, which increased almost 23 percentage points, rocketing from 44.4% to 67.0% in one trading session. Needless to say, options traders were suddenly a lot more uncertain and anxious about AI’s future.

Given the meteoric rise of all things AI, traders have been understandably nervous that the seemingly inexorable trend will suddenly reverse. Naturally, this has led to increased attention and uncertainty regarding the quarterly earnings announcements of AI-related stocks, notably Nvidia (NVDA), Palantir (PLTR), and Advance Micro Devices (AMD). Symptomatically, and as you would expect, the implied volatility of Nvidia and other AI stocks tends to increase before earnings announcements and then fall afterwards, the effect known colloquially as “vol crush.” If you view implied volatility as a measure of future price uncertainty, or anxiety, it makes perfect sense.

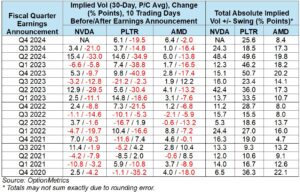

For Nvidia, Palantir, and Advance Micro, vol crush has been an extremely dependable and consistent options strategy. Below, we measured the change in implied volatility (percentage points) in the 10-day period before and after earnings announcements, as well as the total absolute swing over both periods.

Charts displaying the two 10-day periods indicate the significant volatility shifts that have occurred before and after each announcement:

Evidently, vol crush is a very consistent pattern in these three AI stocks; it occurred in 70% of all quarterly earnings announcements in NVDA, PLTR, and AMD since 2020. Total implied volatility swings averaged almost 20 percentage points during the period reviewed, and have been as high as 50.7 (PLTR). Notably, declines tend to be greater than increases; for Nvidia, they occurred 100% of the time; for PLTR and AMD, 82%. Indeed, the five largest negative moves in Nvidia’s implied volatility since 2021 have all occurred within 10 trading days after earnings announcements.

One could make the argument, convincingly, that stocks are susceptible to vol crush when their earnings are favorable or generally within estimates, or at least supporting the prevailing trend. In that case, implied volatility should increase before the announcement as uncertainty builds, but then decrease afterwards as the prevailing trend is confirmed. For the three stocks reviewed, earnings came in mostly within expectations during the period reviewed, a favorable vol crush environment.

For volatility traders, vol crush has been a consistent winner overall. It’s rare that a single option strategy yields consistent and extreme results. Whether this is a symptom of an overdone, hyped market, or just a feature of normal expectations surrounding earnings releases, is open to debate. Whatever the reason, the results stemming from the vol crush effect are undeniable. At the same time, extremely profitable and consistent trades tend to fade over time as investors rush in and mitigate the effects — easy money never lasts. This doesn’t appear to have happened yet, however. Vol crush, especially in the three stocks reviewed, appears to still be a trading strategy that should not be ignored.