Before the unexpected outbreak of hostilities in the Mideast over the weekend, it looked like the rally in crude was finally running out of steam. Unfortunately, crude is now part of the “fear trade” nexus, along with gold, the VIX, and the dollar. If past wars in the region are any guide, the probability of supply disruptions and their consequent effect on oil prices and implied volatility has increased significantly.

Regardless of how you view the situation in the Middle East, a new and significant layer of uncertainty has been injected into energy markets. Uncertainty is one of the main components of implied volatility, and its behavior in energy markets, specifically crude oil, has implications for options pricing and future price trends.

As is common in many other commodities and equities, crude’s implied volatility (whether Brent or WTI) moves inversely to its underlying price. This is especially true during the highlighted periods below:

Source: OptionMetrics

The inverse relationship is also true for energy-related stocks, such as Exxon Mobil (XOM):

Source: OptionMetrics

This is not just a technical quirk that is only of interest to options traders. The effect in crude oil is significant; average implied volatility is almost 4.5 times greater at the lower end of the price curve:

Source: OptionMetrics

Why is this? In equity markets, naturally long positioning leads to a directional bias in implied volatility, with investors sanguine in bull markets but nervous and uncertain when the market turns down. Hence, demand for puts as either a hedge or speculative vehicle increases as the market decreases, increasing implied volatility in the process.

Although similar factors may be at work in crude oil (naturally long producers hedging as prices decrease), other elements specific to the commodity are also present:

1) Asymmetrical daily returns. Charting daily returns (below), it is apparent that they are asymmetrical and are higher and more variable at extremely low prices. Since high and volatile returns are generally indicative of higher risk and uncertainty, implied volatility consequently increases.

Source: OptionMetrics

2) Asymmetric price movement volatility; extreme events. Crude traders tend to believe that prices tend to crash down but drift up. Reviewing the major trends since 2005, as well as the interday changes ($/day) during these periods, this seems to be the case:

Source: OptionMetrics

Source: OptionMetrics

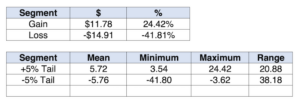

Higher volatility during downtrends is further borne out by the most positive or negative single day extreme movements, as well as by comparing the average of the 5% negative tail versus 5% positive tail of the distribution of interday changes.

Source: OptionMetrics

Traders and investors tend to remember extreme events, and the fear of violent downtrends in crude oil leads to the perception that implied volatility must be increased as prices decline to defray the heightened risk. This leads to the third factor supporting the inverse relationship between price and implied volatility:

3) Increasing risk premiums (implied volatility – historical volatility) at lower price levels:

Source: OptionMetrics

As you can see, the risk premium is significantly larger in the $0.00 to $25 price region. Given the violent price action that has occurred at low price levels (including the shocking move into negative prices in April 2020), the premium seems justified.

4) Institutional options trading dynamics. Option market makers are concerned with maintaining delta neutrality through hedges in the underlying (i.e., in this case, crude futures) or other option positions. In at least one aspect, implied volatility can be viewed as the cost or difficulty in maintaining these hedges. Since the hedges must be continuously adjusted as price levels change, the cost will increase if the market is behaving erratically, gapping up or down from one day to the next, or experiencing abnormally wide daily high/low spreads. The only way to defray the higher costs is to increase implied volatility. As the results above seem to indicate, the conditions that lead to higher hedging costs in crude oil are present when prices reach relatively low levels. Hence, implied volatility tends to increase under these conditions.

The ramifications of the inverse relationship lead to one interesting aspect at high price levels. As noted above, average implied volatility levels at the top end are roughly 4.5 times lower than at the bottom. As such, out-of-the-money options, such as the $100 call, are relatively inexpensive as compared to when underlying prices are low. That will benefit investors contemplating investing in crude oil calls on the back of the current conflict and related supply concerns.

Prajwal Pitlehra, FRE candidate at the NYU Tandon School of Financial Engineering, assisted in the production of this article.