In discussion about an AI bubble, many will point out the domination of the Magnificent Seven and how they account for roughly over a third of the market capitalization of the S&P 500. But two companies on the other side of the world have proven to potentially be a bigger culprit in inflating their country’s equity index.

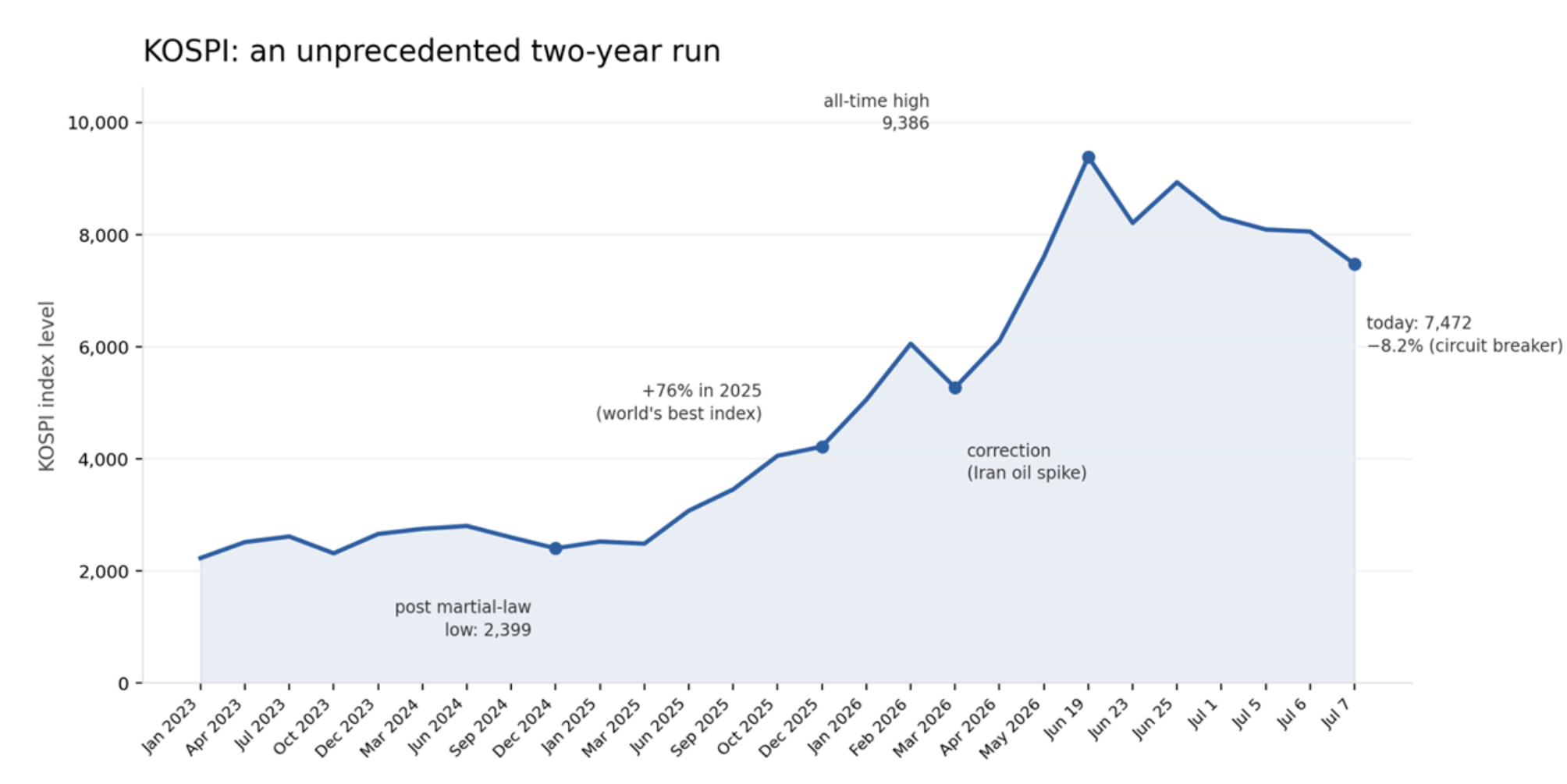

Samsung and SK Hynix own a near monopoly on the production of high-bandwidth memory. They are critical companies to the AI supply chain. Together, Samsung and SK Hynix make up 58% of the KOSPI, South Korea’s equity index that shows the value of all common stock in the country. Samsung has risen around 92% and SK Hynix has risen around 172% year-to-date. These two companies have allowed the KOSPI to have unprecedented growth. For context, since 1985, the KOSPI’s average return is only 8%. 2025 was the largest year in KOSPI growth ever, smashing records every month and ending the year up 75.63%.

Source: Data from KRX (Korea Exchange)—Chart created using Claude AI

Source: Data from KRX (Korea Exchange)—Chart created using Claude AI

The growth in price is not just from speculation but is reflected in growing operating profits. In Q1 2026, Samsung reported ₩57.2 trillion ($38.5 billion) in profit. This one quarter is higher than the entire operating profit of 2025 at ₩43.6 trillion ($30.5 billion). SK Hynix had an even greater 2025, recording ₩47.2 trillion in profit, the first time that the company had profits higher than Samsung’s. In Q1, its operating margin was 72%, an all-time record in the semiconductor industry, which beats out Nvidia.

Despite all this growth in profits, investors are not seeing a proportional increase through dividends. Before the proliferation of AI investments, Samsung had committed itself to paying out ₩9.8 trillion in dividends for FY 2024-26, with a target of 50% of free cash flow. If 50% of free cash flow is greater than 9.8 trillion, investors will get a dividend in excess. If that 50% is less than 9.8 trillion, investors will still get that commitment of 9.8 trillion. Currently, Samsung’s dividend has remained flat, except for a special dividend addition in Q4 2025. Samsung shareholders are placing a bet. They are hoping that major AI investment pledges translate to higher free cash flows that they will see through dividends in 2026.

Source: Chart courtesy of OptionMetrics – Woodseer Global Dividend Forecasting

Source: Chart courtesy of OptionMetrics – Woodseer Global Dividend Forecasting

Samsung is massively increasing its capital expenditures in a way to meet growing memory chip demand. On June 25th, the company made a ₩1,000 trillion ($648 billion) commitment to building AI data centers, chips, and batteries. For full-year capex, the company has made a revision to a record-high ₩110 trillion. These commitments are risky. If memory prices are at their peak right now and pull back in H2 2026, the three-year free cash flow could end much lower than investors could have been expecting after seeing Q1.

SK Hynix may pose an even greater risk for dividend investors. The company’s dividend policy for 2025-27 is a minimum dividend of ₩1500 per share annually, alongside 50% of free cash flow. This is a 25% hike from the company’s previous floor of ₩1200 per share annually. With FY 2026 capital expenditures projected at ₩35 trillion and an estimated operating cash flow of ₩50 trillion, that gives a free cash flow of ₩15 trillion. SK Hynix is different from Samsung in that most of its 2025 shareholder return came from share buybacks, amounting to ₩12.2 trillion. A type of program like this could be cancelled if there was a pullback. There is no obligation for SK Hynix to buy back shares, leaving investors with the ₩1500 commitment and a yield of 0.15% at the current stock price, relatively little as an income cushion.

Source: Chart courtesy of OptionMetrics – Woodseer Global Dividend Forecasting

Source: Chart courtesy of OptionMetrics – Woodseer Global Dividend Forecasting

The risk is not just theoretical and has begun showing up for retail investors. Since the rapid rise of Samsung and SK Hynix, sixteen leveraged ETFs have launched on the Korean market, posting ₩10.4 trillion in trading volume on their first day. 92% of investors in these ETFs are retail investors.

The success of Samsung and SK Hynix has created a speculative bubble in Korea. SK Square, a holding company equivalent to the South Korean Berkshire Hathaway, holds SK Hynix as its primary asset. SK Square has risen 196% in the year just from that asset. Hyundai has risen 49% on the back of Korean market hype, despite a 31% drop in operating income. Typical investments in fundamentals appear to have been put by the wayside.

The investors buying Samsung and SK Hynix through leveraged ETFs and borrowing on margin are not looking for income; they are looking for price appreciation. They are being driven by momentum, and this can reverse quickly. Memory has been historically cyclical, and while today’s demand is real, it is not immune to the same cycles. Tech companies may be forced, in the near future, to slow down data center build-out, likely from regulatory requirements or rising borrowing costs. In that scenario, memory demand could fall; Samsung and SK Hynix will have already spent their capex, leading valuations to also fall, and investors might not have an income cushion to fall back on.

The KOSPI index has been fascinating to follow this year, but dividend investors must stay wary. A fall in memory of demand could gut their valuation, and a lack of income cushion could make it a convincing part of the dividend portfolio.

Written and researched by Thomas Palmer—Thomas is an American Politics and Economics student at Washington and Lee University originally from Mamaroneck, New York