The meteoric rise of 0DTE options has spawned an ecosystem of ETF and overlay strategies centered on harvesting ultra-short-term risk premia, while simultaneously attracting significant retail participation. However, ultra-short option strategies can embed unique risks distinct from traditional longer-dated options, particularly around intraday volatility dynamics and expiration-day mechanics.

Day-of-week effects in short put returns are particularly interesting because Monday expiring options face asymmetric weekend exposure: sellers collect theta decay through Friday’s close but remain exposed to gap risk from Saturday-Sunday news events. The weekend period represents a unique environment where trading halts but information flow continues. Additionally, the reduced ability to rebalance delta exposure over weekends may lead market participants to systematically overprice jump risk in Monday-expiring options, generating an elevated risk premium for volatility sellers willing to hold positions through the weekend gap.

In particular, At-the-money (ATM) short puts with one (trading) day to expiration exhibit extreme gamma exposure as the option’s delta becomes increasingly discontinuous near expiration—small underlying moves generate disproportionately large changes in directional exposure. The liquidity and depth of ultra-short SPX options now enables continuous daily rolling of the Put-Write strategy—selling an out-of-the-money put while posting full cash collateral equal to the strike price. By dissecting across days of the week returns of 1-DTE ATM Put-Write returns on the SPX, we can decompose the contribution of weekend jump risk.

To calculate returns, we utilize 3:45 pm snapshot data from IvyDB US – Intraday and hold position to expiration at the end of the following day. Put options are selected closest to 100 moneyness, and rolled daily. Fully collateralized returns are calculated as premium / (short strike – premium).

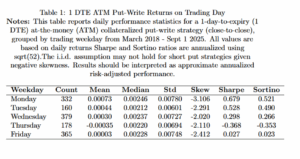

In Table 1 below, we decompose put write returns by day of the week from March 2018- Sept 2025. It should be noted that annualized Sharpe and Sortino ratios are scaled by √52, though this annualization assumes i.i.d. returns—an assumption likely violated by short put strategies given their negative skewness and fat tails—and results should therefore be interpreted as approximate risk-adjusted performance metrics.

Monday expirations generate mean returns of 7.3 basis points—substantially lower than the 24.6 basis point median—with the highest Sharpe (0.679) and Sortino (0.521) ratios among all weekdays, despite exhibiting the most severe left-tail risk (skewness: -3.106). This pattern reveals that while Monday crashes are indeed more extreme when they occur, the premiums collected on Friday for bearing weekend gap risk more than compensate for these tail losses, suggesting that implied volatility systematically overprices weekend exposure even after accounting for the elevated negative skewness.

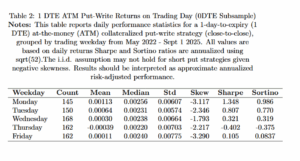

Given the structural transformation in the options market following the widespread adoption of daily expirations in May 2022, examining the post-0DTE period as a distinct regime is warranted. This sub-sample analysis isolates performance in the modern ultra-short maturity ecosystem, where continuous rolling strategies are now feasible and market microstructure has meaningfully diverged from the pre-2022 regime.

Table 2 reveals an intensified Monday outperformance pattern alongside persistent stability in median returns across weekdays. Monday mean returns of 11.3 basis points now exceed other days by even wider margins than the full sample, generating exceptional risk-adjusted metrics (Sharpe: 1.348, Sortino: 0.986) despite the highest negative skewness (-3.117) observed across any day. Median returns remain tightly clustered between 22-26 basis points across all weekdays. This reinforces that Monday’s dominance derives entirely from heightened premiums—weekend gaps that do occur are less severe than the elevated Friday implied volatility would suggest especially in the 0DTE period.

Next it is important to evaluate the statistical significance of our findings. Bootstrap resampling repeatedly samples our actual return data with replacement to build confidence intervals without assuming any particular distribution shape—crucial since short put returns exhibit extreme negative skewness and fat tails that violate normality assumptions. We focus on median daily returns rather than means because the median represents the “typical” outcome. This allows for statistically valid inference about central tendency while avoiding the distortions that crash events create in standard tests.

To investigate whether Monday options exhibit systematically different performance, we bootstrapped the median returns of fully collateralized short ATM put positions across different weekdays. In the full historical sample, Monday median returns exceeded other weekdays (aggregate median) by 1.95 basis points, though this difference was not statistically significant (95% CI: -0.95 to 4.18 bps, p > 0.05). However, the picture changes dramatically in the modern 0DTE era. Since the inception of daily expirations, Monday short put returns have outperformed other weekdays by 3.25 basis points—a difference that is now statistically significant (95% CI: 0.48 to 6.94 bps, p < 0.05).

Given the statistical significance, it makes sense to quantify the economic effect of weekend jump risk. We conduct a backtest in the 0DTE era of 1DTE ATM Put Write strategies of all trading days versus trading days excluding Mondays (Friday – Monday close). Beginning the test in 2022 allows for a like for like comparison between the strategies, as prior to 2022, ejecting Monday expirations would comprise 33% of tradeable days.

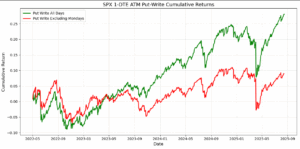

Table 3 provides the performance statistics of the strategies. Excluding Monday expirations from the 1-DTE ATM put-write strategy results in a substantial deterioration of risk-adjusted performance, with the annualized Sharpe ratio declining from 0.725 to 0.331—a reduction of approximately 54%. This degradation occurs despite similar volatility levels (9.86% vs. 9.68%), indicating that Monday expirations contribute disproportionately to mean returns while not materially increasing risk. The cumulative return falls from 28.07% to 8.94% over the sample period, suggesting that the weekend risk premium—captured via Monday-expiring options that span the Saturday-Sunday non-trading period—represents a critical component of short-dated put-write profitability in the post-0DTE regime.

The chart below plots the cumulative returns of each strategy. The exclusion of weekend trading reduces cumulative returns by approximately 68% (from 28.07% to 8.94%), demonstrating that weekend risk premia—earned through options spanning the Saturday-Sunday non-trading period—account for nearly two-thirds of the strategy’s total profitability despite Mondays representing only one-fifth of trading days.

The concentration of two-thirds of put-write profitability into Monday expirations demonstrates that weekend volatility harvesting has become a significant source of returns in the 0DTE era, as Friday implied volatility systematically overprices the realized weekend gap risk. This finding suggests calendar timing has significant implications for ultra-short-dated gamma and volatility harvesting strategies. For investors, this means that systematically avoiding Friday positions could substantially deteriorate risk-adjusted returns in put-write and volatility-selling strategies. The key takeaway is that the short term variance risk premium in equity options has become concentrated in specific calendar patterns, which has meaningful implications on overall strategy performance.