Garrett DeSimone, PhD

Oscar Shih

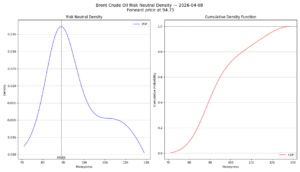

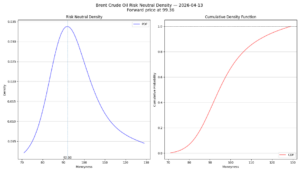

Following the collapse of US-Iran peace talks in Pakistan, the Brent crude RND has shifted meaningfully. The mode migrated from 89 to 92 in moneyness, and the forward itself rose from $94.75 to $99.36 — reflecting Trump’s announcement of a naval blockade in the Strait of Hormuz. The distribution has flattened, with peak density dropping from 0.037 to roughly 0.034, as probability mass distributed into the tails. Notably, the right-tail plateau between moneyness 110-120 that we identified last week — which we interpreted as residual ceasefire skepticism — has disappeared. The density now decays smoothly through the right tail, suggesting the market has moved past the binary ceasefire-holds-or-collapses framing and is instead pricing the current state of affairs — an active naval blockade with ongoing but uncertain diplomacy — as the new baseline rather than a tail scenario.

The mode moving toward ATM reinforces this interpretation. Last week at 89, the market was saying the forward was an overshoot that would likely revert. At 92, the gap between the most likely outcome and the forward has narrowed — the market is increasingly treating elevated crude prices as justified by fundamentals rather than as a temporary conflict premium. The smooth right tail means the extreme escalation scenarios (prolonged Hormuz closure, infrastructure strikes) are no longer being priced as a distinct regime separate from the base case — they’ve been absorbed into the central distribution. Put differently, what was a tail risk last week is now just the market’s reality.