Since ancient times, gold has been regarded as an enduring store of value. Buoyed by its push toward record highs last January, supporters cast it as an all-purpose hedge — against inflation, geopolitical risk, and broad-based uncertainty, all while touting its superior performance. Many therefore argue that gold belongs in any diversified portfolio.

But does gold’s glittering image hold up against its historical record?

As with most assets, gold’s performance as an asset or hedging vehicle is inconsistent and highly dependent on the period under review. Positive real interest rates, a strong dollar, or major global economic events often conspire to prevent gold from acting as a reliable hedge or performing well in relation to other assets.

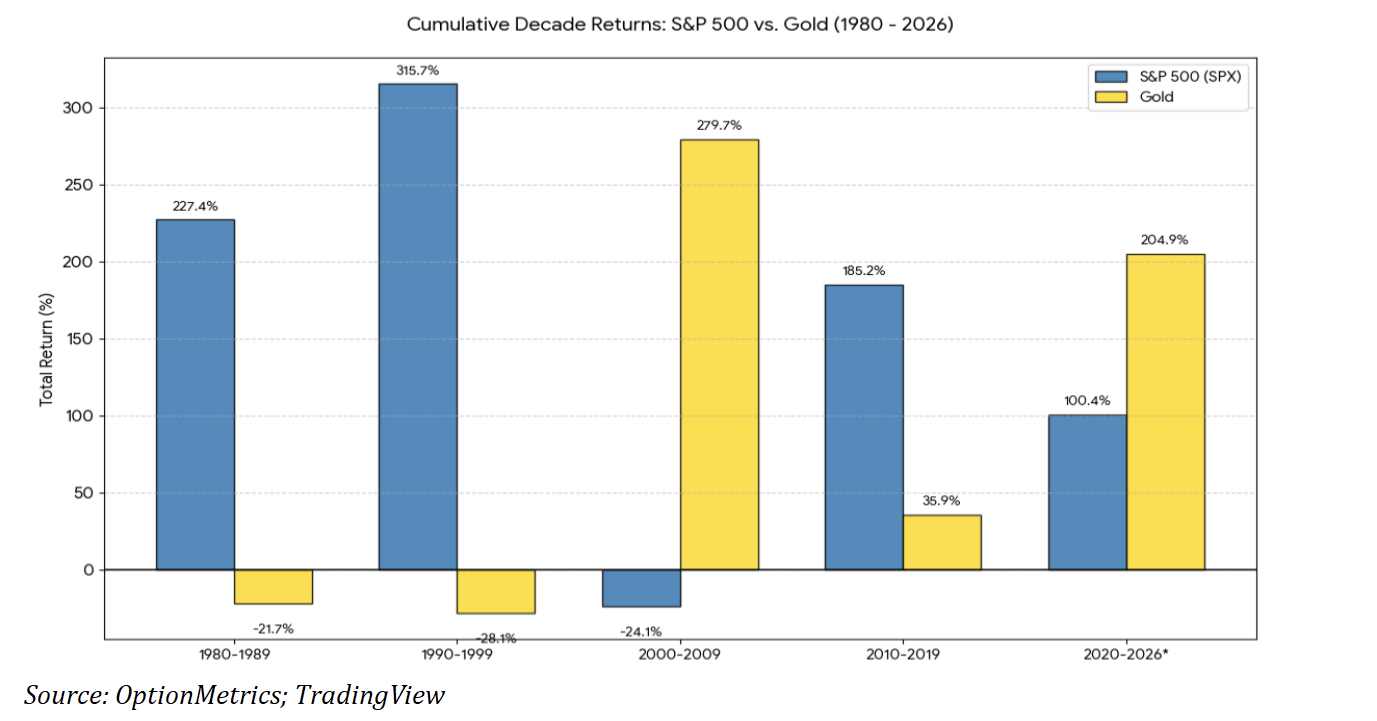

To begin, let’s review the relative performance of gold (continuous futures) to the S&P (SPX). The chart below compares their returns since 1980:

Gold’s performance since 2000 has been impressive, returning 1553%. That’s over 4 times the S&P’s total return of 369%. However, the period from 1980 – 2000 tells a very different story. To recap, gold experienced a boom in the late 1970’s from nearly a decade of double-digit inflation and geopolitical uncertainty, peaking at $850 in early-1980. After the Fed slammed on the brakes by raising interest rates, the metal entered into two decades of declining performance and wound up losing 51% by 2000. At the same time, the S&P exploded and finished the same period up 1261% (SPX). Gold’s $850 high was not broken until almost 28 years later in early-2008.

Gold’s record as an inflation hedge is also inconsistent. Two periods stand out: 1980–2000 and 2022. Although inflation rose at a slower pace from 1980 to 2000, the overall price level still more than doubled; over the same period, gold fell almost 51%. Similarly, in 2022, CPI inflation reached 8.0%—the highest reading in 41 years—while gold was down 0.28% for the year. In both episodes, gold did not act as an effective inflation hedge.

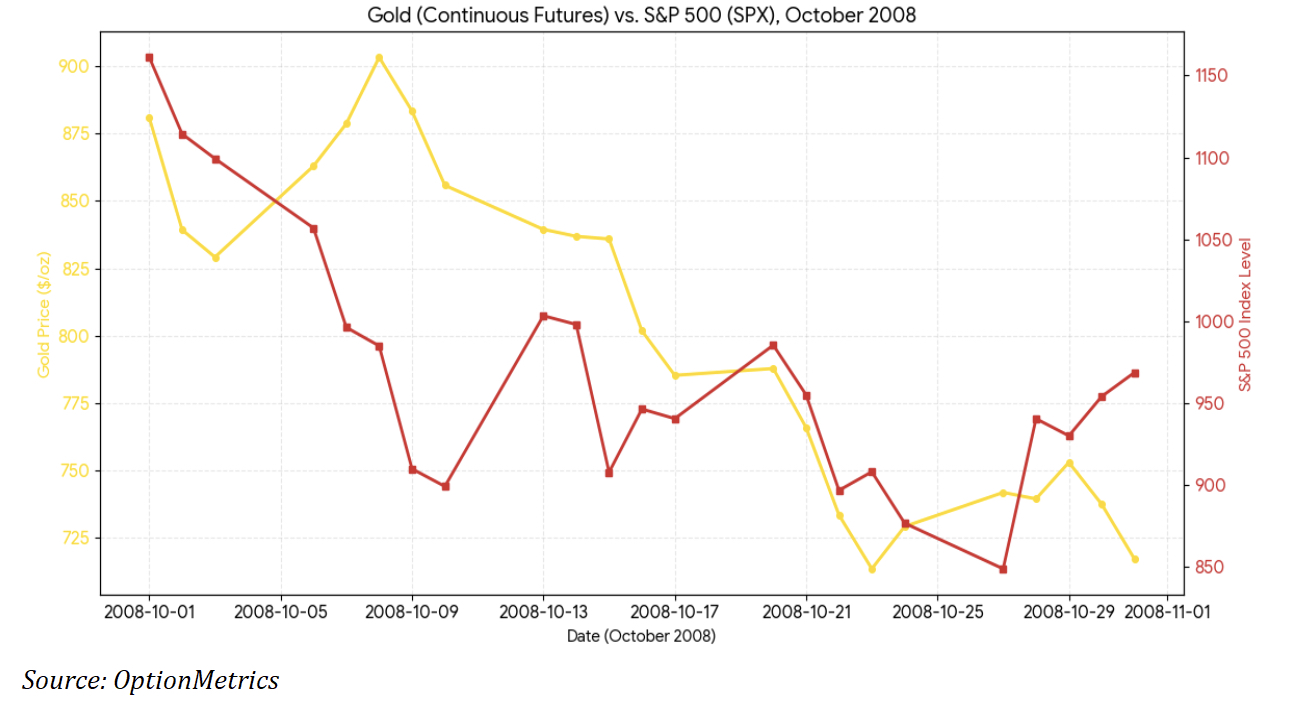

Gold’s performance history as a left-tail hedge against geopolitical or economic crises is also mixed. During October 2008, the first month of financial crisis and the most significant downturn since the Great Depression, a massive flight to liquidity engulfed gold as well as all other assets. The SPX fell 16.6%; at the same time, gold fell 18.6% (see chart below). Although gold subsequently rallied, it ended the year up a paltry 3.1% while the S&P ended the year down 37.6%. Evidently, gold failed as a safe-haven hedge during the most severe period of the crash.

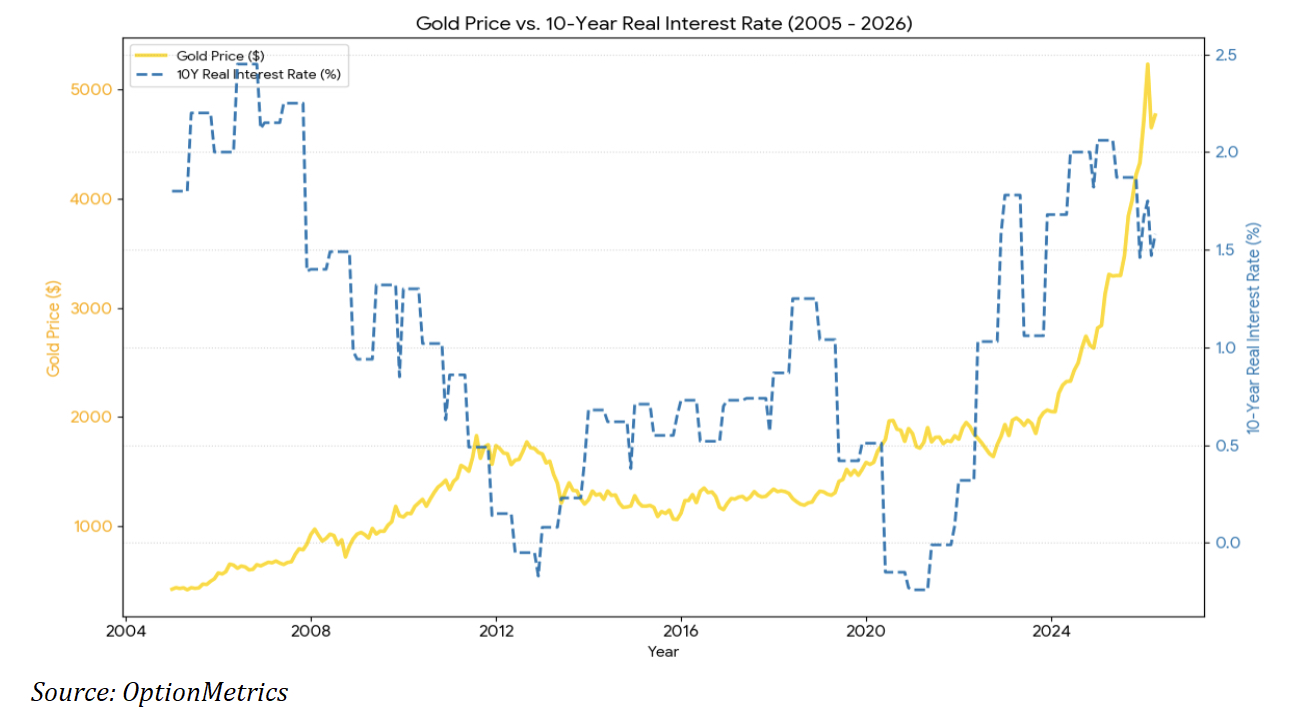

The metal’s record as a hedge against real interest rates is also inconsistent. Conventional wisdom holds that since gold is a non-interest-bearing asset, as real rates rise, investors tend to flee gold in search of yield elsewhere, and vice versa. However, as the chart below indicates, this isn’t always the case. Gold’s latest climb to new all-time highs was accompanied by relatively high real interest rates. Evidently, retail participation, geopolitical unrest, anticipation of higher inflation and currency debasement, and sheer momentum, were enough to swamp the effect of high real interest rates.

After reviewing the historical record, it is clear that gold’s performance is highly regime- and period-dependent. As we demonstrated, the 1980–2000 period differs markedly from 2000–2026. The fundamentals that affect gold—inflation, real interest rates, the dollar, central banks, and geopolitical and economic shocks—can matter a great deal, but their impact is uneven across economic and risk regimes.

Gold advocates who omit earlier periods may be falling prey to two logical fallacies common in market analysis: confirmation bias and recency bias. In other words, they remember the episodes when gold acted like a hedge and delivered strong relative performance but ignore the extended stretches when it did not. Like most investors, they also tend to overweight recent events and price history. This pattern is not unique to gold — commentary on other asset classes often falls into the same trap. Historical analysis is only useful when viewed objectively and without preconceived notions.