Wars in the Mideast and Ukraine, oil prices up sharply year-to-date, continued tariff and trade uncertainty, a private credit mini-meltdown, rumblings about an AI bubble, and economic uncertainty at record levels—any one of these could lead to the conclusion that we should be experiencing sharply higher volatility like that seen during extreme financial crises.

In a previous blog entitled Are the Markets More Volatile Now? (February 18), written before the outbreak of the war in Iran, I concluded that perceptions of increased volatility—especially those portrayed in the press and social media—were not supported by traditional volatility metrics such as a sustained rise in negative daily returns, higher volatility risk premiums, or a persistent jump in the VIX.

How has the war changed the volatility picture? The answer is not that obvious and has implications for current VIX levels.

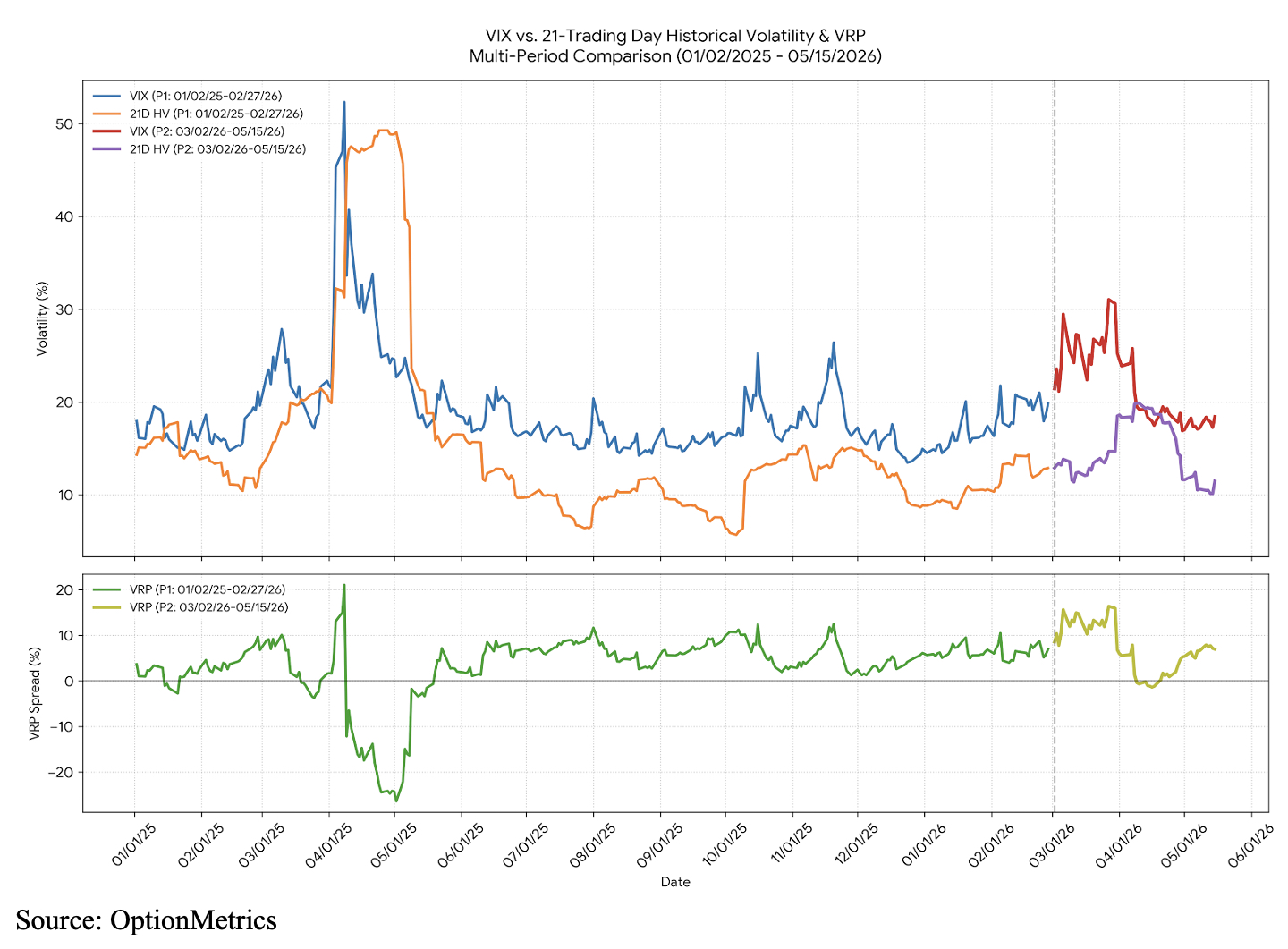

To find out, we compared the VIX index, 21-day historical (realized) SPX volatility, and the volatility risk premium (known as VRP or the difference between market expectation of future volatility versus actual volatility) for the periods before and after the war started (01/02/2025 – 02/27/2026) versus 03/02/2026 – 06/03/2026. In this case, we defined the volatility risk premium as the VIX minus 21-trading day realized volatility. Since the VIX (implied volatility) is forward-looking and historical volatility only looks backward, the VRP can sometimes produce useful insights on how the market is pricing risk and downside insurance.

Below is a chart comparing the three metrics over the two periods in question:

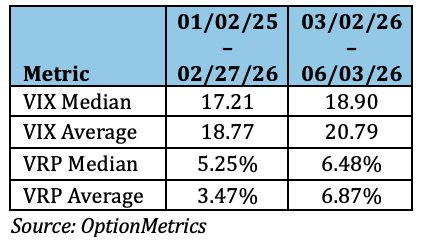

Although the VIX (blue/red line above) has pulled back from its mid-March highs, its average and median levels are still higher than in the pre-war period. In addition, the VRP (lower panel above) is also higher as is on average almost twice that of the pre-war level:

Although the VIX (blue/red line above) has pulled back from its mid-March highs, its average and median levels are still higher than in the pre-war period. In addition, the VRP (lower panel above) is also higher as is on average almost twice that of the pre-war level:

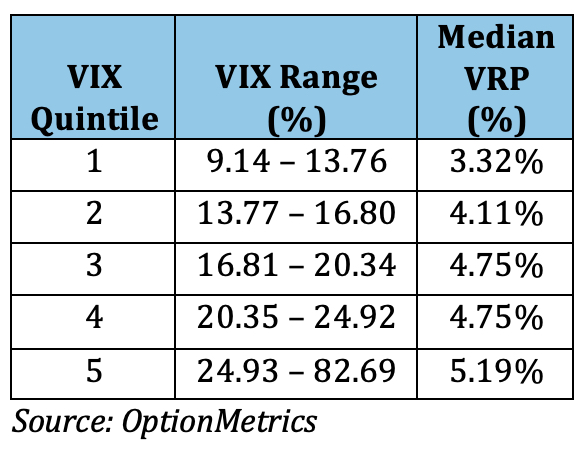

On a longer-term basis, arranging the VIX into quintiles since 1996 provides another indication that the current VRP is abnormally high compared to not only the previous period but to its long-term average and median levels:

The VIX has primarily been in the upper quintiles since the war began. The current VRP of 5.60 (06/03/2026) is significantly higher than the medians for both those quintiles, indicating that options are pricing in high levels of risk and uncertainty. Unless war-related uncertainty eases, the risk premium is likely to stay elevated, implying that today’s relatively moderate VIX should not be mistaken for calm.