How do investors price dividend uncertainty, known as the dividend risk premium, into equities and ETFs? This is something that can now be more easily and accurately assessed using OptionMetrics’ new IvyDB Implied Dividend. Implied dividends are risk-neutral dividends derived from option prices at various maturities. These implied dividends are often discounted compared to realized dividends, with the spread representing the “premium.”

This premium compensates for the risks associated with changes in firms’ dividend policies. There is a natural market demand to hedge dividend risk, particularly from pension funds and insurers, that rely on stable dividend streams for long-term obligations. During deteriorating economic conditions, this premium tends to widen as companies face the risk of cutting dividends.

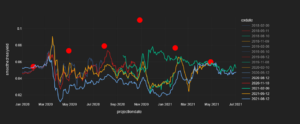

This pattern was evident across several securities during the pandemic. In the chart below, we plot ExxonMobil (XOM). The colored lines represent the annualized implied yield for various ex-dates, while the red dots represent realized yields at ex-dates.

XOM Implied Dividend

Source: OptionMetrics IvyDB Implied Dividend

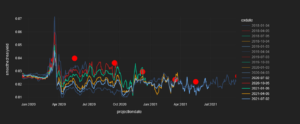

Our estimates show that during the height of the Covid-19 pandemic, XOM implied yields were discounted by 2 to 5%. However, this spread disappeared by May 2021, as the market recognized that XOM would not be cutting its dividend. We observe a similar pattern with JP Morgan (JPM) dividends.

Source: OptionMetrics IvyDB Implied Dividend

Aside from reflecting returns on dividend-based strategies, the dividend risk premium acts as a barometer of market sentiment. A rising premium suggests greater market uncertainty or pessimism about future earnings. It also offers a useful input for valuation models, particularly for companies with uncertain dividend payments. Consequently, incorporating the dividend risk premium into analysis can improve both investment decisions and valuation assessments.