Geopolitics are dominating the markets, and crude oil is front and center. The war in Iran, and the related closing of the Straits of Hormuz, have led to the most severe supply constraints since the oil embargoes of the 1970s. Consequently, crude oil has been experiencing sudden and extreme price swings and triple digit volatility. Many commentators have called this “unprecedented.” That’s understandable given recent events, but as we will show below, it is incorrect.

To illustrate the point, we review the return, volatility, and monthly spread history of crude oil futures (WTI) going back to 2005.

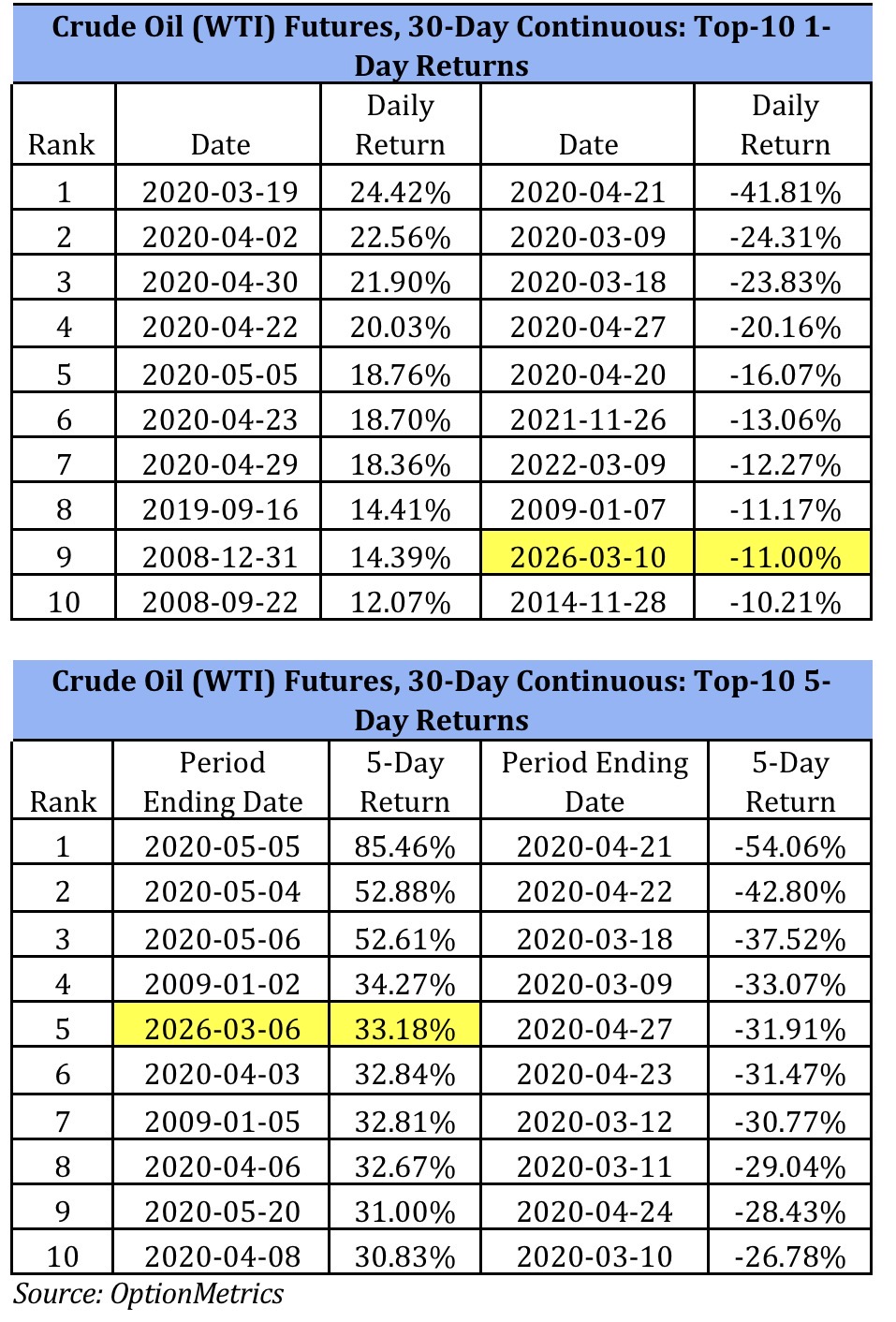

First, we compile the top-10 largest price swings measured over 1- and 5-day periods:

As you can see, March, April, and May of 2020 dominated the findings, with only two results from the current period. One should not underestimate their significance, however, since the current situation is only about three weeks old and still has significant potential for continued oil price shocks.

As you can see, March, April, and May of 2020 dominated the findings, with only two results from the current period. One should not underestimate their significance, however, since the current situation is only about three weeks old and still has significant potential for continued oil price shocks.

Today’s price changes, although certainly extreme, appear to be nowhere near, nor as shocking, as what occurred during the previous period. After all, April crude oil (WTI) settled at negative $37.63 on April 20, 2020, a truly unique event in the history of exchange-traded commodities.

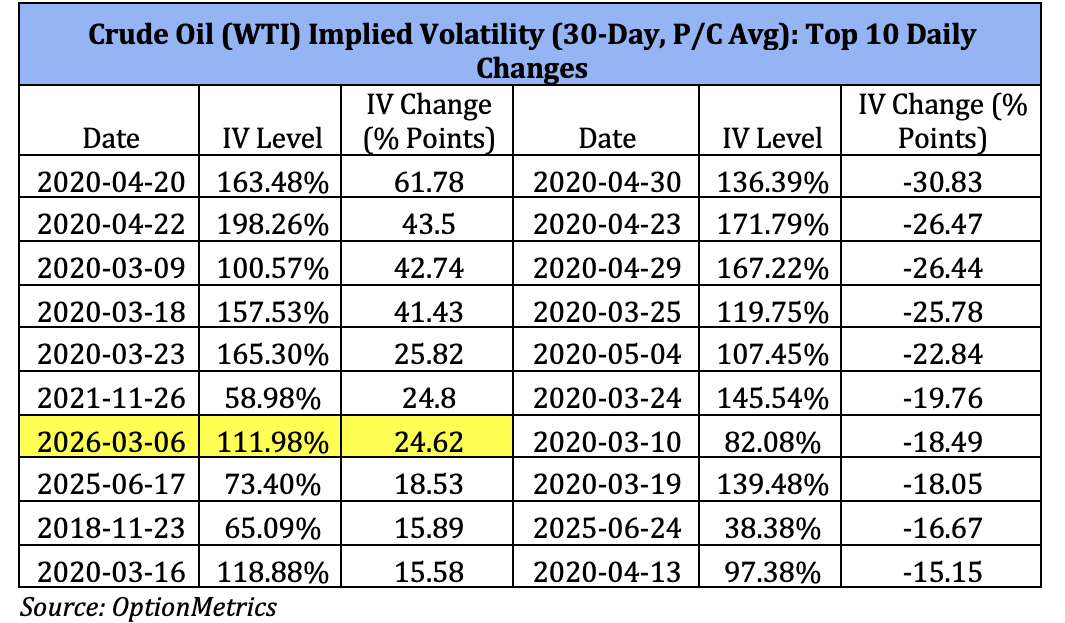

Second, we reviewed the top-10 one-day changes in implied volatility. Not surprisingly, the results are similar, with only one date from 2026 making the list:

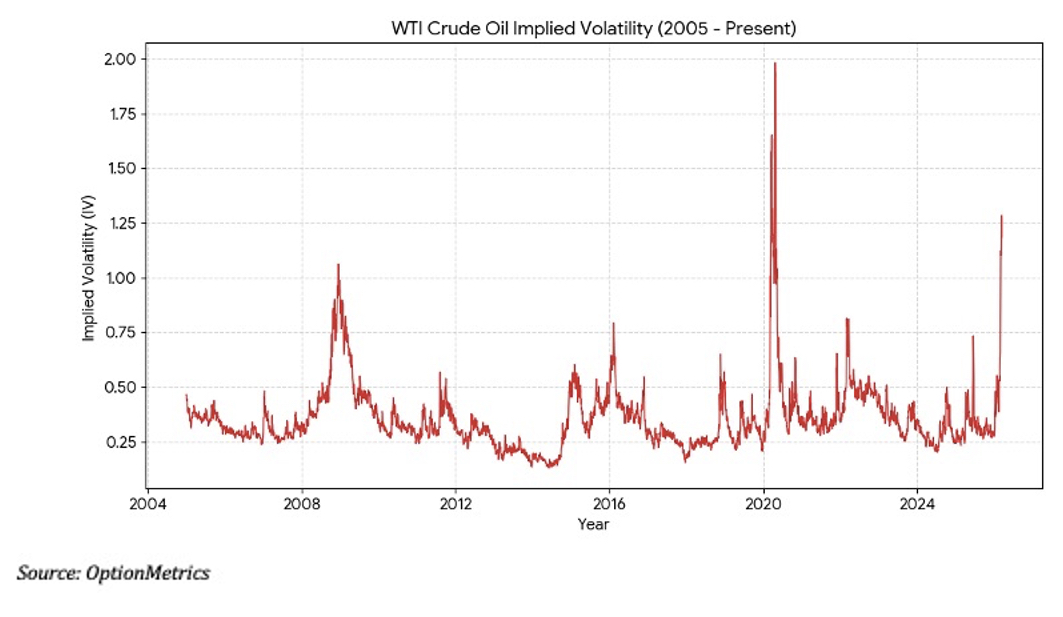

We also reviewed the absolute level of implied volatility to see how it compares to other shocks. Again, March and April 2020 registered considerably higher implied volatility than in the current period. Continued supply shocks from the Iran war may force volatility much higher, but so far they haven’t.

Implied volatility over 100% indicates extreme stress and uncertainty. Luckily, and despite its reputation for extreme volatility, levels over 100% in crude oil are relatively rare. Since 2005, there have been only 46 days in which it has occurred. Of these, 38 occurred in 2020 and 6 so far this year.

And finally, we examined intermonth spreads, specifically the 6-month to 1-month spread. Reflecting the severe shortage of physical barrels, crude oil is currently backwardated, i.e., nearby contracts are priced higher than deferred. It’s a common condition in commodities with limited storage or supply disruption. As you can see below, the first half of 2022 had similar levels of backwardation.

Current conditions in crude oil are certainly chaotic, uncertain, and prone to severe movement in price, volatility, and monthly spreads. Given the situation in the Straits, that is to be expected. However, by the metrics we reviewed above, March, April, and May of 2020 were more statistically volatile. Of course, the war is only three weeks old, and the previous period spanned 90 days. In addition, WTI and Brent benchmarks somewhat conceal the spikes in more regional, and volatile, indexes centered in the Gulf States. Given the extreme geopolitical uncertainty and the potential for unexpected shocks, the current period could potentially yet turn out to be the most volatile ever.

Current conditions in crude oil are certainly chaotic, uncertain, and prone to severe movement in price, volatility, and monthly spreads. Given the situation in the Straits, that is to be expected. However, by the metrics we reviewed above, March, April, and May of 2020 were more statistically volatile. Of course, the war is only three weeks old, and the previous period spanned 90 days. In addition, WTI and Brent benchmarks somewhat conceal the spikes in more regional, and volatile, indexes centered in the Gulf States. Given the extreme geopolitical uncertainty and the potential for unexpected shocks, the current period could potentially yet turn out to be the most volatile ever.