On July 9th, President Trump imposed a 50% tariff on copper imports, effective August 1. This followed an executive order last February launching an investigation into how copper imports may affect national security. The August 1 deadline now looms, and the obvious question is whether the President will extend it or modify the new tariff level.

By way of background, copper is often dubbed “the new steel,” and is a critical component in construction, electronic products, defense, and transportation. To date, approximately 50% of US domestic consumption is imported, mostly from Canada and Peru, in the form of refined copper. China, cited by the administration as effectively controlling the market, accounts for about 45% of global refinery production, but only 1% of total US imports.

The new copper tariffs are meant to spur domestic production and refining capacity and address national security concerns. It’s going to be an uphill fight; copper production doesn’t just expand at the flip of a switch. Building and permitting a copper smelter can take more than five years. Mining the metal has an even longer lead time; it takes an average of 29 years for a new copper mine to begin production. That’s too long for most investors.

The anticipation of tariffs on commodities tend to distort normal locational price differences, as well as supply chains. Case in point: since last February, a massive amount of copper has been shipped to the US in anticipation of the impending tariff. Record disparities between New York and London prices have resulted, and specialized hedge funds with the necessary experience to ship and warehouse copper have been the main beneficiaries. In a market in which a good trade makes $100/ton profit, gains of over $1000/ton have been reported. Last February, when blanket European-wide tariffs were announced, similar locational price disparities appeared in gold and set off a London to New York shipping frenzy. Apparently, announcing tariffs that will go into effect months later is the hedge fund gift that keeps on giving.

Given the President’s penchant for tariffs, some amount was expected, just not as high as 50%. That drove copper up 13% in the front month futures contract, an all-time high and, reportedly, the largest daily increase since 1968. Copper is now up over 45% year-to-date, behind only palladium (41.7%), and platinum (58.5%) for the largest commodity price increase so far this year.

Despite the President’s assertion that the deadline will not be extended, his history of delaying, cancelling, or modifying allegedly immutable dates merits skepticism (TACO, again?). First, their effectiveness, as noted above, is debatable (although that has not been an impediment previously). Second, the details of the tariff still have not been settled, even with the August 1 deadline only days away. It’s still unclear whether the tariffs apply to refined metal, semi-finished product, or copper ore (one possible compromise is to allow imports of refined copper but impose tariffs on semi-finished products only, such as wires, tubes, and strips). In any case, details matter.

On the other hand, tariffs on two other metals, steel and aluminum, were imposed at 25% last March and then doubled to 50% in June, with no modification or nod to their effectiveness or distorting effects. The UK was the only country excluded.

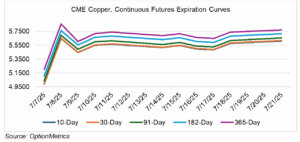

In addition, the copper market itself, specifically the shape of the futures curve and its role as a leading indicator of economic conditions, may be indicating that the August 1 deadline might indeed be hard and fast.

Below are CME copper continuous futures prices for various maturities, displayed before and after the July 9th tariff announcement. As you can see, each maturity moved roughly parallel to the other, despite the rally. If the market believed that the tariffs would be delayed past the August 1 deadline, then only the nearest maturities should increase relative to the later expirations. In other words, the curve should flatten and move towards backwardation (near expirations more expensive than deferred). However, the influx of massive amounts of copper into the US in anticipation of the tariffs may be mitigating that effect, artificially distorting the market.

There has been another distortionary effect as well. Regardless of whether the tariffs go into effect on August 1 or not, there is one side effect that should not be overlooked. Historically, since copper is used as an input to so many products and processes, analysts used it as a leading indicator of economic activity. In fact, commodity insiders refer to it as “Dr. Copper” (“it’s the only metal reputed to have a Ph.D. in Economics”). And yet, since tariffs first became a possibility last February, copper’s price action has had everything to do with tariffs and little to do with future economic activity. Dr. Copper is out of the office.