From the War in Ukraine, to supply chain issues, rising energy prices and inflation, and Fed rate hikes, 2022 was an eventful year, to say the least. It was also characterized by heightened volatility in the US and Europe, as a result, compared to 2021’s more muted vol.

Volatility peaked in June 2022 in the US and subsided in Q4, as likely due to softer inflation readings relative to the summer. And Europe also contended with heightened volatility in 2022, in part due to globally high inflation and hawkish central bank policies.

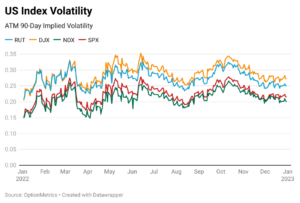

The charts below show Index Volatility in the US and Europe, and are followed by observations alongside key events in 2022 and volatility in the markets.

- Volatility across major US indices heightened in 2022 in response to high inflation and aggressively hawkish Fed policies

- Volatility peaked in June as a result of an 8.6% May CPI print, the largest 12-month increase since the period ending in December 1981

- Volatility subsided in Q4 as likely due to softer inflation readings relative to the summer

- Volatility in Nasdaq and Russell indices exhibited a significant 5% spread against their S&P 500 and Dow Jones counterparts. This suggests that growth, tech and small cap equities will remain riskier into 2023

- Europe also contended with heightened volatility in 2022 in part due to globally high inflation and hawkish central bank policies

- Europe’s overdependence on Russia for energy likely led to elevated volatility compared to other regions as a result of supply shocks from the Russia-Ukraine War in Q1

- Volatility peaked in early March amid fears of a cutoff of Russian energy supplies

- A decrease in volatility in Q4 coincides with a softening dollar

- Inflation numbers are largely widespread in European countries, with some countries (such as Hungary, Latvia, Estonia, Lithuania, Ukraine) as high as 20%