Given the significantly increased tensions due to the war in the Middle East and its unexpected nature, the reaction of the VIX has been muted, to say the least. In the two weeks following the unexpected outbreak of war in the Middle East, the VIX staged a disappointing 4 point rally to reach a near term high of 21.70 on 10/20. The war served to accelerate the bullish trend already in place since the YTD low of 12.82 was made on September 14. Although it rose to levels not seen since the beginning of the regional banking crisis last March, VIX gains were short lived.

After the initial shock of the unexpected war in the Middle East, the VIX quickly drifted back into the mid-teens, familiar territory, giving up all of its gains a mere 16 trading days after the beginning of the war. That leads to a question: is the current market too complacent and was the relatively brief upside move in the VIX a harbinger of things to come? Or will any upside move be unsustainable absent certain factors? In a previous blog, The VIX Isn’t Broken!, I reviewed some of the main drivers behind the VIX — uncertainty, risk premiums (in this case, 30-day realized – 30-day implied volatility), and daily direction and changes in the SPX — and concluded: a) that these interrelated factors must be present if increases in the VIX are to be sustained, and b) that the VIX remains a relevant indicator of volatility and market sentiment.

How does the VIX’s reaction to the Middle East war stack up versus other significant economic and political events, such as the 2008 financial crisis, the COVID pandemic, the war in Ukraine, and the regional banking crisis? And what does it say about what could drive the VIX to higher levels on a more sustained basis?

The degree to which the various factors driving the VIX influence the index is not constant but varies depending on the most recent market and political developments. For example, the uncertainty factor, as reflected in the risk premium, dominated the VIX’s movement in the period immediately following the outbreak of war in the Middle East. That being said, its increase and range was less than what occurred in previous crises:

Source: OptionMetrics

Risk Premium Quartiles

| Regime | 1st Quartile | 2nd Quartile | 3rd Quartile | 4th Quartile |

| 2008 Crisis | -1.91% | 3.83% | 7.96% | 24.39% |

| Stable Period | 1.11% | 3.68% | 5.43% | 13.14% |

| COVID Period | 1.61% | 5.55% | 10.88% | 19.38% |

| Ukraine War | 2.85% | 1.30% | 5.07% | 13.46% |

| Regional Banking Crisis | 2.99% | 4.36% | 7.04% | 11.05% |

| Israel-Hamas Conflict | 4.24% | 5.78% | 7.19% | 8.78% |

Source: OptionMetrics

Indeed, after its initial and unimpressive rally to 21.71, the VIX has been on the defensive and its risk premium has collapsed:

Source: OptionMetrics

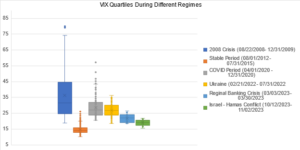

Overall, the VIX’s reaction to the war was muted, at best, especially when compared to previous crises:

Source: OptionMetrics

VIX Quartiles

| Regime | 1st Quartile | 2nd Quartile | 3rd Quartile | 4th Quartile |

| 2008 Crisis | 24.75 | 31.54 | 44.66 | 80.86 |

| Stable Period | 12.98 | 14.07 | 15.88 | 26.25 |

| COVID Period | 23.93 | 27.29 | 31.77 | 57.06 |

| Ukraine War | 23.87 | 26.88 | 30.18 | 36.45 |

| Regional Banking Crisis | 19.47 | 22.02 | 23.83 | 26.52 |

| Israel-Hamas Conflict | 17.71 | 19.27 | 20.44 | 21.71 |

Source: OptionMetrics

Most recently, the shock of the war and its resulting uncertainty as a factor driving the VIX is receding, and the inverse relationship of the VIX to the SPX is reasserting itself:

Source: OptionMetrics

Apparently, VIX traders believe that the war will not spread regionally and will remain contained, with little direct impact on the SPX, petroleum supply, or global financial conditions. Ignoring this possibility, they have driven the VIX lower in reaction to the most recent SPX rally. However, the war is in its early days and its medium to long term ramifications are not at all clear.

VIX levels in the mid-teens seem to be overly discounting the probability that the war could metastasize into a broader, more serious, and influential conflict. Such expansion could lead to significantly higher levels as the uncertainty factor comes to the fore. As such, and with the VIX trading in the mid-teens, the upside/downside risk of a short VIX position does not seem to be favorable at this time.

Prajwal Pitlehra, a FRE candidate at the NYU Tandon School of Financial Engineering, assisted in the production of this article.