By Abhi Gupta and Manajit Gogate

There has been lively debate surrounding the future of Cathie Wood’s ARK innovation fund (ARKK) actively managed portfolio. The discussion is centered around whether the valuations of the constituent stocks may be at least partially driven by ARK’s large ownership in the companies.

We explore this, as well as other aspects of ARKK, below, and find that:

- ARKK’s fund inflows/outflows appear to provide great systematic risks for its portfolio of small cap companies, potentially offsetting the diversification benefits of ETFs and Indices.

- The options market appears to be mispricing ARKK’s, and its constituents’, options prices based on implied correlation metrics.

Several pieces have been written about ARKK’s concentrated positions in small cap companies over the last year, including this from Morningstar. Given this, ARKK’s fund inflows/outflows provide great systematic risks for these small cap companies that comprise it, potentially offsetting the diversification benefits of ETFs and Indices.

Could the options market be mispricing the diversification benefits of holding ARKK compared to its constituent stocks? In this post, we look at risks in ARKK portfolio and the potential for mispricing in the options market, as well as potential arbitrage trading opportunities in implied correlation trading.

First, it’s important to highlight ARKK’s concentrated positions in small market cap companies. As shown below, companies with market cap less than ~10 billion account for nearly 25% of ARKK’s portfolio, resulting in ARKK being one of the largest institutional owners in these stocks.

Source: ARKK website and OptionMetrics (as of 2022-01-21)

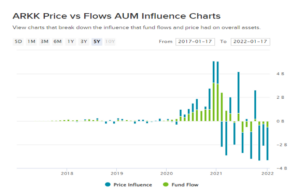

Next, we look at ARKK price influence versus flows influence to assess the impact of fund flows on ARKK’s performance.

Source: ETF Database

The above chart from ETF Database, indicating ARKK price influence versus flows influence, suggests that ARKK fund flows has outsized impact on its performance. From the start of 2020, there have only been five out of 36 months where fund flows and price show different trends. Of those five with different trends, three were due to a sharp fall in Tesla stock price during February of 2020 and February-March 2021. It is important to note that Cathie Woods has not made claims that her ARKK portfolio provides diversification benefit. However, we can quantify ARKK’s diversification benefit by using an implied correlation measure between ARKK and its constituents.

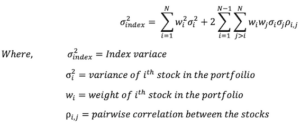

Implied Correlation

CBOE releases the implied correlation Index for S&P 500 Index and Top 50 constituents by market capitalization of S&P 500 index. The average correlation is calculated based on Harry Markowitz’s portfolio theory as follows:

The average implied correlation is obtained by simply averaging of all of the pairwise correlations ρ_(i,j) in the formula above. The CBOE uses three-month at-the-money (ATM) implied volatilities of the S&P 500 index and individual stocks to calculate the average implied correlation.

The Markowitz’s portfolio theory also tells us variance of portfolio of uncorrelated assets is less than that of the sum of individual securities due to diversification benefits. However, during the troubled times, correlation between the securities increase and diversification benefit disappears.

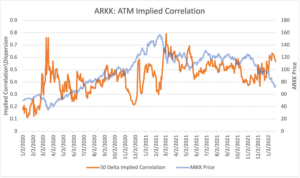

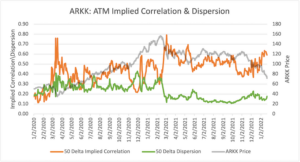

In the chart below we study implied correlation between ARK Innovation ETF (Ticker: ARKK) and its portfolio stocks.

Source: OptionMetrics

The chart above shows the ATM 91 – day implied correlation (orange line) for ARKK imposed over ARKK’s price (blue). As expected in March 2020 during the start of the Covid-19 pandemic, implied correlation spiked to 0.8 and was oscillating between 0.20 and 0.50 for the rest of 2020.

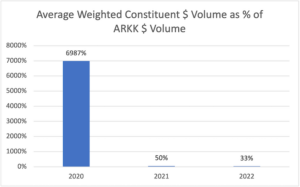

While ARKK price started moving south with the start of 2021, implied correlation jumped from 0.40 to the 0.6 band. The increased volume in ARKK options compared to its constituent stocks also appears to have played an important role in explaining the jump in the correlation (see below chart: Average Weighted Constituent $ Volume as % of ARKK $ volume).

If we compare the implied correlation of ARKK to that of the S&P 500 Index’s, or Cboe® Implied Correlation® Index (COR3M) from CBOE’s website, the results are telling. At the beginning of Jan 2021, COR3M was around 34 (or 0.34 correlation), while ARKK implied correlation was at around 0.5. Currently, as of January 20th, 2022, COR3M is at 45 (or 0.45 correlation) while ARKK implied correlation is at 0.60, observing a difference of 0.15, similar to that observed during January 2021. We might assume this difference is due to the liquidity premium in the options market between ARKK and its holdings. However, the low levels of implied correlation for ARKK compared to the S&P 500 Index seems to suggest that the market is pricing in some diversification benefit in holding ARKK portfolio when there appears there may be no such benefit.

Source: CBOE

You might wonder, why we started comparing the ARKK and S&P 500 implied correlations starting in 2021 and not in 2020? It is because during 2020 ARKK’s AUM showed exponential assets under management (AUM) growth and involvement of the WallStreetBets (WSB) crowd in the market might have distorted the pricing of implied correlation. By the end of the 2020, ARKK AUM plateaued before starting a downward trajectory toward the end of 2021. So, for the most part, most of 2021 appears to provide more realistic comparison points.

This is evident by dollar volume of options on constituent stocks and ARKK. There is an order of magnitude difference in the traded volume in ARKK from 2020 to 2021.

Source: OptionMetrics

This vast difference in liquidity of ARKK can explain the shift in implied correlation and dispersion charts from March 2021.

We hypothesize that this disparity in the market pricing of diversification benefits (even with liquidity premium) and actual portfolio condition may provide an arbitrage opportunity for dispersion trading in ARKK and its constituents’ options.

The dispersion is simply the difference between weighted implied variance of the constituent stocks and implied variance of index.

Naturally, correlation and dispersion are at opposite ends: the higher the correlation between the index components, the lower the dispersion and vice versa.

Source: OptionMetrics

As illustrated in the research above, there appears to currently be low diversification benefits of holding the ARKK portfolio. As a result, a short dispersion trade (i.e., long correlation trade) might be interesting to consider at this time. This type of trade might include a long straddle on index (ARKK) and short straddles on the index constituents. The risk factor in executing this trade is liquidity in ARKK and constituent stocks.