Implied volatility (IV) is often treated as the market’s best estimate of future uncertainty and risk. But just how accurate is it in predicting actual future price variation? And is there a broader implication to the answer?

To find out, we reviewed SPX and VIX data going back to 1996 (7655 trading days). We then calculated the forward-looking volatility risk premium (VRP), defined here as the VIX index on any day minus the future realized volatility (i.e., the annualized standard deviation of daily SPX lognormal returns) over the next 30 days (approximately 21 trading days). Note that this is the opposite of the exercise in which past realized results are compared to the current implied volatility, mixing backward-looking metrics (historical realized volatility) with forward projections (implied volatility).

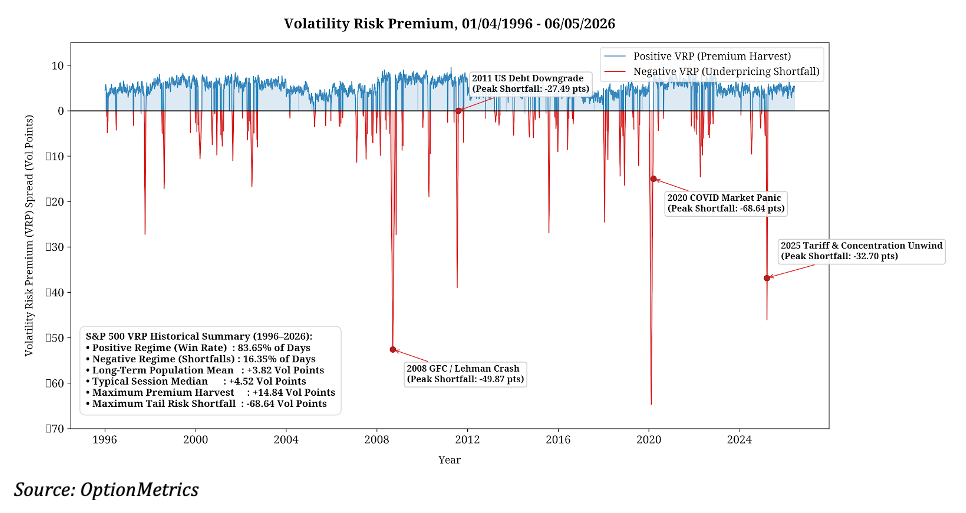

The chart below displays the results:

As you can see, the VRP is generally positive (blue line), indicating implied volatility typically exceeds forward realized SPX volatility. In this sample, that was true 83.7% of the time, with an average premium of 3.82 percentage points and a mean of 4.52. With an average and median VIX of 20.15 and 18.5 respectively over the same period, the gap between realized and projected volatility is almost 20%. Evidently, option sellers have a built-in safety margin – usually.

As you can see, the VRP is generally positive (blue line), indicating implied volatility typically exceeds forward realized SPX volatility. In this sample, that was true 83.7% of the time, with an average premium of 3.82 percentage points and a mean of 4.52. With an average and median VIX of 20.15 and 18.5 respectively over the same period, the gap between realized and projected volatility is almost 20%. Evidently, option sellers have a built-in safety margin – usually.

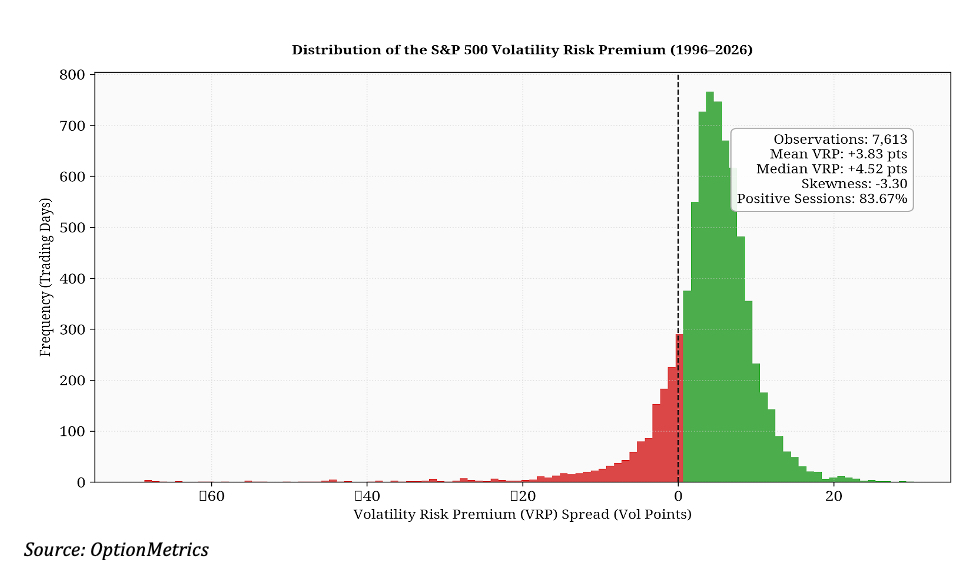

That is not always the case. During periods of extreme stress, the normally positive VRP can invert and turn sharply negative (red line above). As indicated by the red line above, the major financial shocks of the last 30 years all produced a relatively short period in which implied volatility failed to accurately predict realized results. Unsurprisingly, the results of a market shock can be extreme, with the VRP ranging from -22 during the Long Term Capital Management (LTCM) panic (09/1998) to -68.64 at the height of the pandemic shock (02/2000). These and other extreme negative movements reflect the extreme left tail and skewness of the VRP distribution:

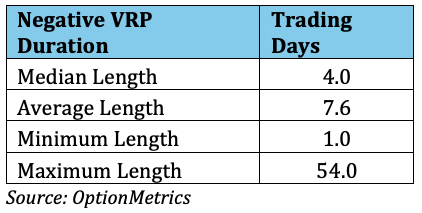

Although the longest episode of negative VRP occurred during the 2008 financial crisis, most negative VRP shocks lasted only four trading days, typically reflecting a brief realized volatility spike before markets stabilized.

Although the longest episode of negative VRP occurred during the 2008 financial crisis, most negative VRP shocks lasted only four trading days, typically reflecting a brief realized volatility spike before markets stabilized.

Judging by the forward-looking VRP levels described above, it seems that implied volatility is an imperfect indicator of future realized price variation. However, although true, it conceals a broader point. Across the full sample, the VIX generally exceeded subsequent 30-day realized SPX volatility, confirming that option prices typically include a persistent volatility risk premium. The premium reflects the compensation investors require for bearing volatility risk and for providing protection against extreme left-tail events. Conversely, when the VRP turns negative, the premium is no longer sufficient to compensate for prevailing risk. In that case, it may also signal that a risk regime change is underway. In either case, the forward-looking volatility risk premium can be a valuable tool in assessing the market’s appetite for risk.