By: Garrett DeSimone and Oscar Shih

On April 8th, a two-week ceasefire between the US and Iran was announced just 90 minutes before President Trump’s deadline for Iran to reopen the Strait of Hormuz. Risk appetite snapped back across asset classes. The speed of the move underscored a point the options market had been making for weeks: the conflict premium embedded in crude was fragile, and most of the probability mass in the risk-neutral distribution sat well below the forward price even at the height of the crisis.

For options traders, geopolitical supply disruptions like the ongoing Iran-US conflict are unique because they introduce a regime-dependent payoff structure: either the disruption persists and prices remain elevated, or a resolution — diplomatic or military — returns supply to market and prices revert toward pre-conflict fundamentals. Futures options markets reflect this directly by pricing a mixture of states of the world. The probability the market assigns to escalation versus resolution can be inferred from option prices through the risk-neutral distribution, which reflects the market’s implied likelihood of different price outcomes at maturity. It’s important to note that these options deliver a future, which can sit above or below the spot based on the structure of the market, which indicates the mass of the probability distribution typically will sit above or below the current spot. At a high level, we extract these implied probabilities as follows:

- Construct a standardized volatility surface using OptionMetrics’ proprietary arbitrage-free methodology.

- Fit the strike dimension with a spline to generate a continuous set of strikes.

- Apply the Breeden–Litzenberger approach to recover the implied probability density for each strike. Implied probabilities are then plotted based on forward moneyness.

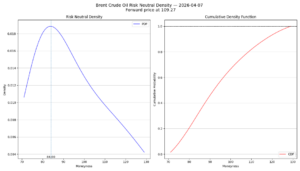

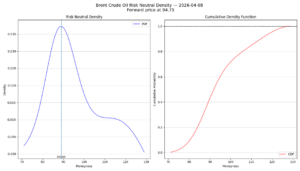

Below are the risk-neutral densities (RNDs) for Brent crude oil on April 7 and April 8, extracted from options on the April futures contract with 21 days to expiration. The shift between the two densities captures how the options market repriced the conflict in a single session.

Source:OptionMetrics

On April 7, the RND was wide and flat, with a peak density of roughly 0.027 centered at a mode of approximately 83 in moneyness — 17% below the forward. The left tail was particularly heavy, with density at moneyness 70 starting around 0.015 — indicating the market viewed a sharp retracement as plausible even at the height of the crisis. The mode sitting so far below the forward told a clear story: the options market appeared to percieve the most likely outcome was well below the prevailing futures price, suggesting the forward was being pulled upward by a relatively low-probability but high-impact right tail.

By April 8, following the ceasefire announcement, the distribution had narrowed considerably. Peak density rose to approximately 0.037 — nearly 40% higher — and the mode shifted rightward to around 89 in moneyness. Probability mass migrated out of both tails and back into the body of the distribution. The left tail thinned dramatically, with density at moneyness 70 falling to near zero.

Perhaps the most notable feature of the post-ceasefire RND is the persistent plateau in the right tail between moneyness 110 and 120, where the density hovers around 0.010 rather than decaying smoothly. This shelf-like structure suggests the market is pricing a mixture of two regimes: a primary scenario in which the ceasefire holds and crude settles near or below the forward, producing the concentrated peak around 89, and a secondary scenario in which the ceasefire collapses and the escalation resumes, generating a diffuse band of elevated outcomes above the forward. The plateau, rather than a clean second mode, reflects the fact that the escalation scenario does not have a single price target — it encompasses a range of possible disruptions of varying severity. We define the implied probability of conflict escalation from the current ceasefire as the probability of Brent crude settling more than 5% above the forward price — the region of the density beyond the inflection point where the RND transitions from smooth decay into a persistent plateau. As of April 8, this probability stands at approximately 15-20%.

Taken together, the one-day shift reveals a market that moved swiftly to reprice the central tendency — the mode jumped six moneyness points in a single session — while retaining a degree of structural skepticism in the right tail. The ceasefire reduced uncertainty but did not eliminate it. The options market is treating the truce as the most probable path forward, but is maintaining a standing premium for the possibility that it doesn’t hold.