By: Oscar Shih

Volatility skew serves as a widely recognized measure of investor perception of downside jump risk. It reflects the market’s directional bias – or the extent to which traders are more concerned about the underlying asset rising or falling. A positive skew suggests a bearish sentiment, as traders pay more for put options than call options.

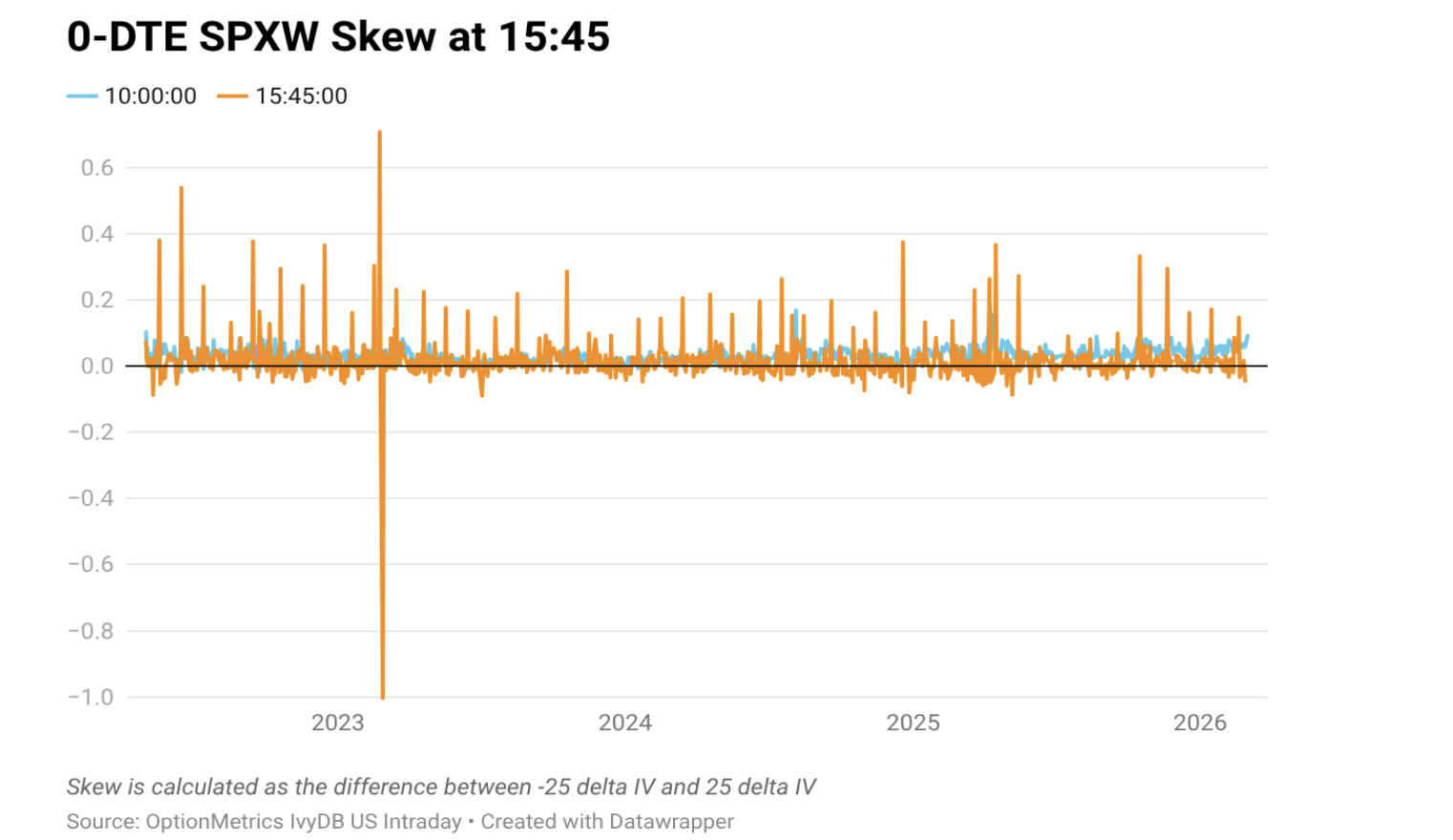

Using volatility surface data from OptionMetrics IvyDB US – Intraday, we can uncover market asymmetry at 10:00, 14:00 (2:00 pm), and 15:45 (3:45 pm) ET. We compute the zero-day-to-expiration (0-DTE) skew at 15:45 ET solely with SPXW (S&P 500 Weekly) options. Specifically, the skew is defined as the difference between the implied volatility at the 25-delta put and the implied volatility at the 25-delta call along the 0-DTE slice of the volatility surface. Generally, the SPX volatility skew is positive due to institutional demand to hedge downside risk.

The chart below plots the 0-DTE skew at 15:45 starting from May 2022, when Cboe started listing 0-DTE options. A notable pattern emerges: the skew exhibits periodic spikes that coincide with the third Thursday of each month— one day before the traditional monthly options expiration date. We further decompose the skew by third and non-third Thursday at two different timestamps – 10:00 and 15:45 ET, and the summary statistics are below.

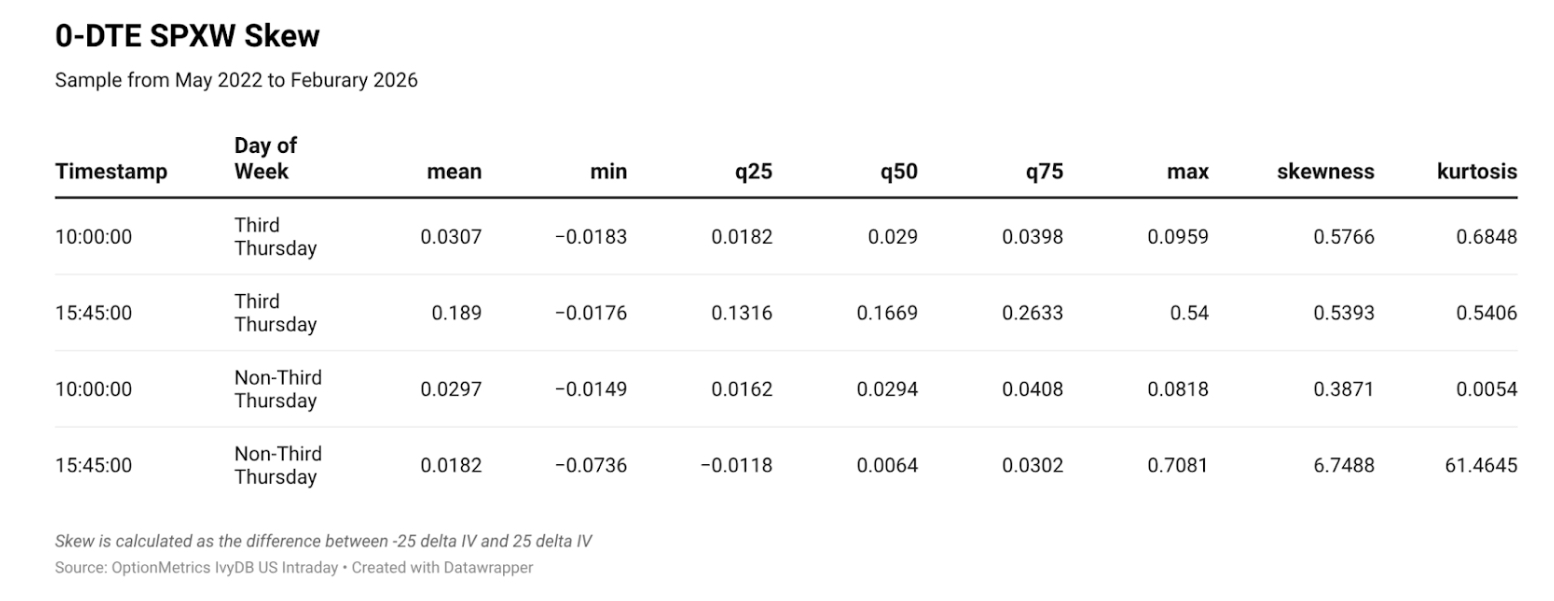

We further decompose the skew by third and non-third Thursday at two different timestamps – 10:00 and 15:45 ET, and the summary statistics are below.

Across all groups, the mean and median skew are positive, confirming the premium for downside hedging. However, the magnitude differs significantly by time of day and expiration cycle. At 15:45 on the third Thursday, the median 0-DTE skew reaches 0.17 – over four times larger in magnitude compared with only about 0.03 in other timestamps. Notably, the spike doesn’t appear earlier in the trading session. The skew at 10:00 on the third Thursday remains similar across all groups. The effect, therefore, appears concentrated in the final 15 minutes of trading on the day before monthly SPX options expiration.

Third Thursday options expiration is unique in that it is the only day of the month where two large expiration cycles converge simultaneously — weekly Thursday contracts expire at the close while standard monthly Friday contracts carry near-terminal gamma with one day remaining. This overlap creates the highest aggregate gamma outstanding of any day in the monthly cycle, concentrated at the strikes where institutional hedgers have accumulated put protection throughout the month. Critically, this is not an informational phenomenon — it is a mechanical consequence of open interest structure, where the calendar alignment of two expiration cycles produces a gamma concentration that would not exist on any other trading day.

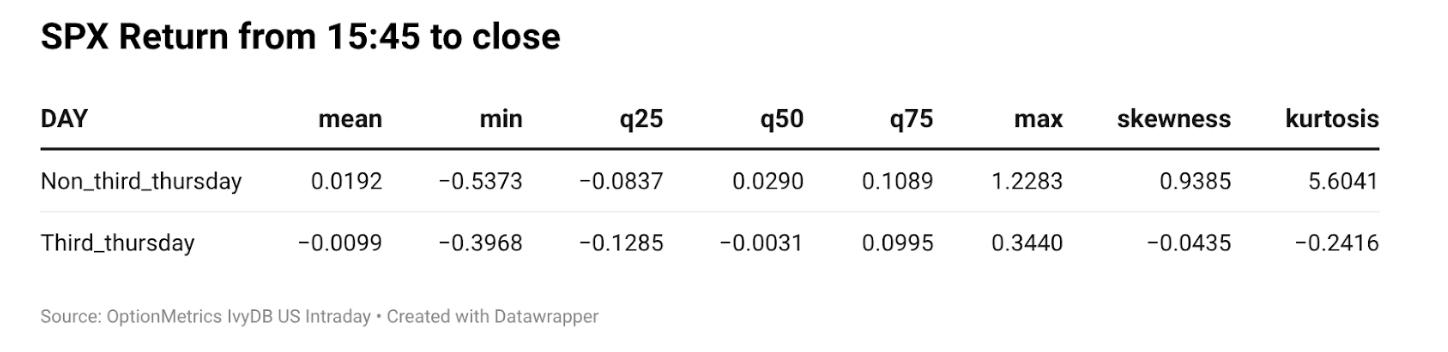

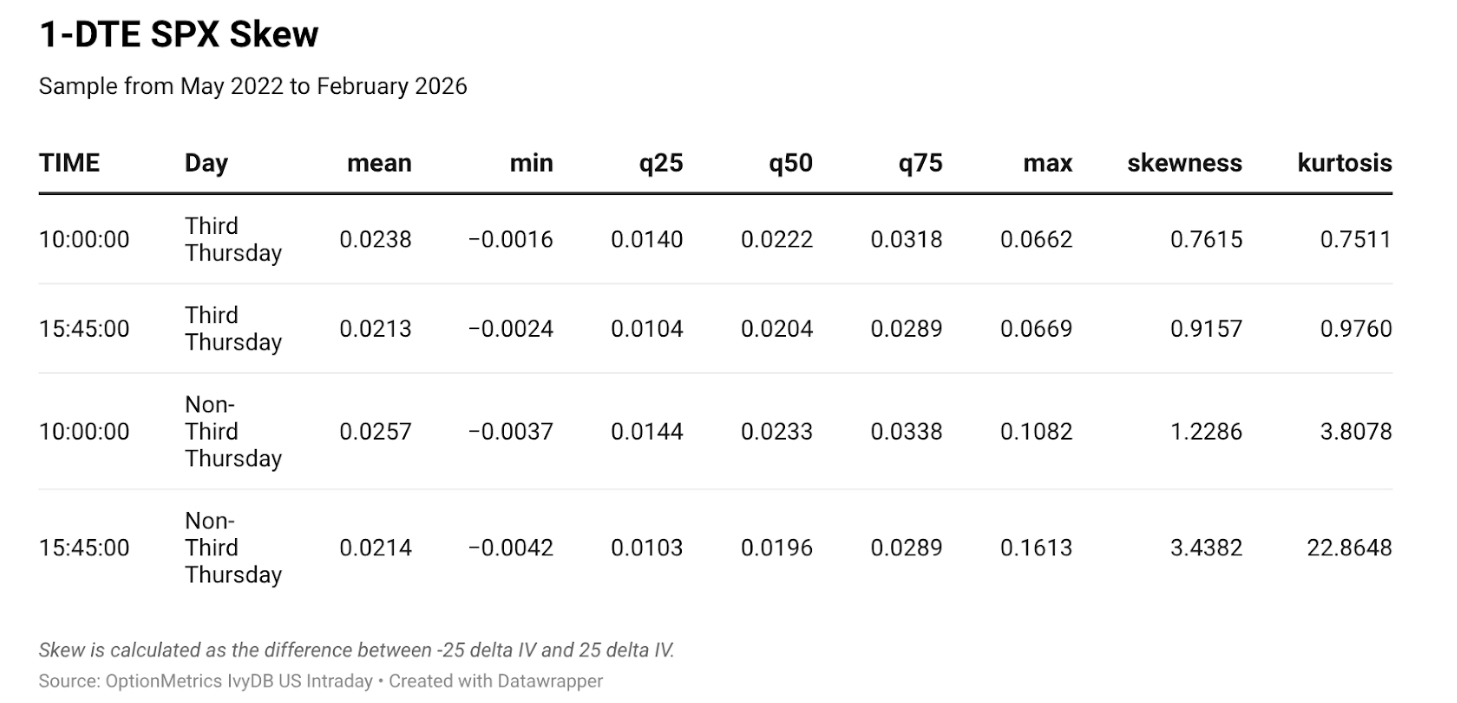

Dealers who are net short puts across both expiry cycles face destabilizing hedging dynamics – any initial selling pressure into the close forces dealers to sell the underlying to maintain delta neutrality, creating a feedback loop that amplifies small directional moves into negative average realized returns. The table above quantifies this effect through SPX returns measured from 15:45 ET to market close using index-level prices. On third Thursdays, both the mean and median realized SPX returns are negative, compared to non-third Thursday observations when both are positive. The negative skewness of the return distribution further supports the hypothesis that dealers’ delta-hedging activity is one of the systematic drivers of adverse price realization during this window. The unhedgeable nature of terminal gamma on the daily weekly contracts means dealers demand significant compensation for bearing pin risk near high open interest strikes, showing up as elevated implied volatility skew in zero-days-to-expiration options. Notably, this skew elevation does not appear in the one-day-to-expiration monthly contracts, where residual time value preserves the ability to dynamically hedge. The table below details the SPX 1DTE skew at the same window as the 0DTE skew, but it shows similar levels across different timestamps.

On third Thursdays, the convergence of two expiration cycles creates an unusually high gamma concentration that mechanically drives elevated 0-DTE skew in the final 15 minutes of trading – a phenomenon distinct from any other day in the monthly options cycle. This skew spike, accompanied by negative SPX returns near the close, reflects dealers’ delta-hedging pressure.