The SEC’s recent approval of Monday and Wednesday expiries for single-stock options marks a significant evolution in the options market. Until now, daily expirations have been the exclusive domain of major index products and ETFs. The extension of 0-DTE trading to individual stocks like those in the MAG7 raises an important question: are investors being adequately compensated for the additional risks unique to single-name short-dated options?

We can gauge this compensation through the variance risk premium (VRP), which measures the difference between what the options market implies about future volatility and what actually materializes. When implied variance consistently exceeds realized variance, option sellers are being compensated for taking on volatility risk — and the VRP captures the size of that compensation. A persistently positive VRP signals that the market routinely overpriced variance, making it a useful tool for comparing how much sellers are paid for bearing risk across different securities.

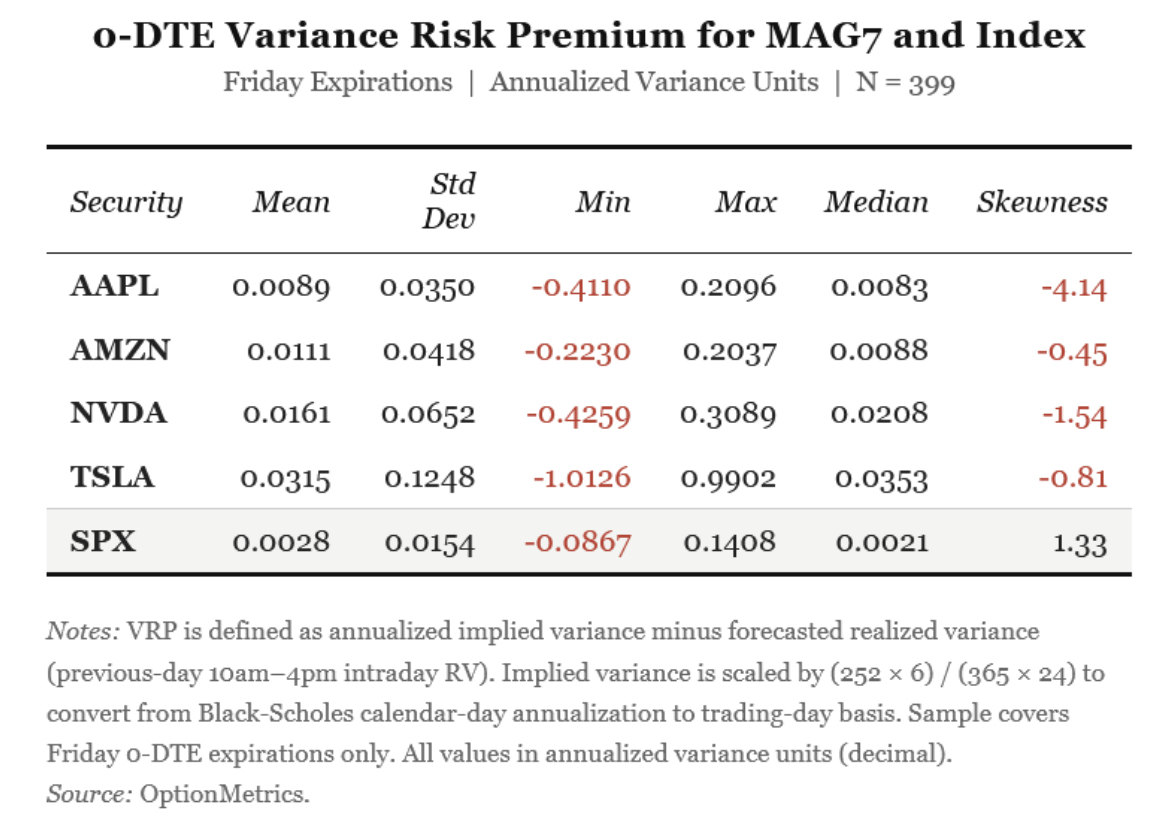

Using OptionMetrics’ IvyDB Intraday, we calculate the ex-ante 0-DTE variance risk premium for select MAG7 stocks and the SPX index over the period 2018 to present. The VRP is defined as the difference between implied variance — derived from ATM options on the 0-DTE surface at 10 am EST — and forecast realized variance, proxied by the sum of squared log returns from 10 am to close on the previous trading day. It is worth noting that VRP is not directly tradeable; it serves as a measure of prospective compensation available to variance sellers at the open, rather than a realized profit series. Prior to the recent introduction of Monday and Wednesday expiries, single-name 0-DTE options were only available on Fridays. To ensure a like-for-like comparison between single names and the index, we restrict our analysis strictly to Friday expirations across all securities.

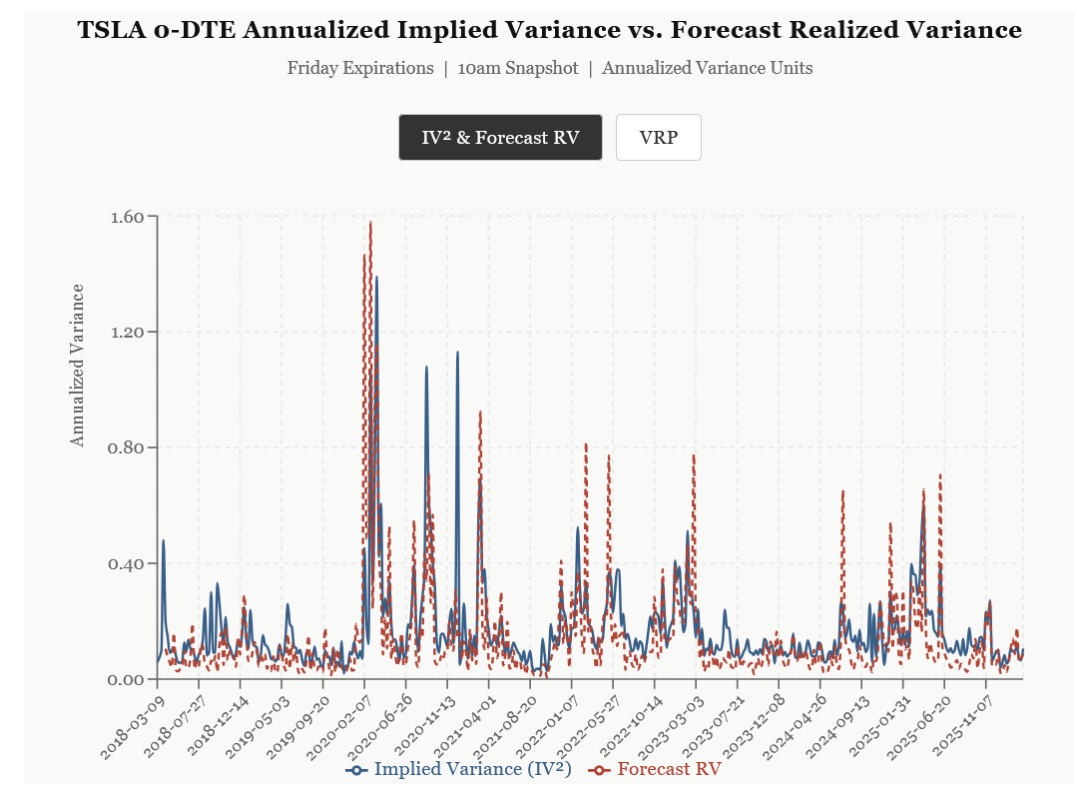

The chart below plots annualized implied variance against forecast realized variance for TSLA across our sample period. Forecast realized variance is simply the previous days’ intraday realized variance. In most periods, implied variance exceeds the forecast — consistent with a positive VRP and reflecting the premium the market charges for bearing intraday variance risk. Episodically, however, forecast realized variance spikes above implied variance, representing periods where the previous day’s realized volatility was elevated relative to what the market priced into 0-DTE options at the open.

Looking across multiple securities, the table presents ex-ante 0-DTE variance risk premiums for four large-cap equities and the S&P 500 index (SPX) over 399 Friday expirations. Across all securities, mean and median VRP are positive, confirming that implied variance systematically exceeds forecast realized variance and that option sellers are prospectively compensated for bearing variance risk at the intraday horizon. Single names exhibit substantially larger VRP in absolute terms, with TSLA commanding the largest premium (mean: 0.0315, median: 0.0353), followed by NVDA (0.0161), AMZN (0.0111), and AAPL (0.0089). This ordering broadly tracks the volatility level of each security. The index VRP is markedly smaller — SPX mean of 0.0028 and median of 0.0021 — reflecting the diversification of idiosyncratic risk at the index level.

The most striking difference between single names and the index lies in the skewness of the ex-ante VRP distribution. All single names exhibit negative skewness, ranging from -0.45 (AMZN) to -4.14 (AAPL), indicating a left-tailed distribution where occasional large forecast realized variance events significantly exceed implied variance — the hallmark of short volatility tail risk. SPX, by contrast, exhibits positive skewness of +1.33, suggesting the index variance seller faces a more symmetric distribution where implied variance more consistently exceeds the forecast. This divergence implies that while single names offer larger raw premiums, they carry meaningfully greater tail risk, and the index short volatility may be more attractive on a risk-adjusted basis.

While this analysis is specific to Friday expirations, it offers a meaningful look into how 0-DTE variance risk is priced across MAG7 stocks and the index. Single names carry significant idiosyncratic risk that is costly to hedge, and this is reflected in their consistently larger median VRPs relative to SPX. However, the pronounced negative skewness across single names signals that this premium comes with a catch — tail events where realized variance dramatically overshoots implied variance are more frequent and severe than with the index, creating a meaningfully higher probability of outsized losses.

In short, single-name short volatility appears lucrative on average, but the asymmetric downside risk warrants caution for any strategy seeking to harvest it systematically.